Numbers Matter: Defense Acquisition, U.S. Production Capacity, and Deterring China

INTRODUCTION

In conflict, the ability to sustain the demands of combat over the long haul separates the victorious from the vanquished. To triumph, a nation requires ample weapons and stores and the capacity quickly to produce more. If that capacity and capability are uncertain, its deterrence abilities are weak. Aggression becomes appealing to its enemies.

What is the current state of production capacity across America’s industrial base, compared to adversaries such as the People’s Republic of China, which the U.S. military calls our principal pacing threat? The conflict in Ukraine has illuminated inadequate numbers of weapons in the U.S. inventory, from artillery shells to anti-aircraft missiles, due to an undersized workshop for war, a predicament the unexpected necessity to backstop Israel after the October attacks exacerbated. Overall, U.S. military systems are too old and few. Its magazine stocks are too low.

The United States will need a magnitude more of the weapons systems and production capacity to deter war in the Pacific and prevail if necessary. China’s leaders will only be deterred if they know the United States can sustain protracted conflict for months to come: destroying the People’s Liberation Army’s ships and satellites; devastating their naval, air, and missile formations; and choking off their pivotal supply chains.

Historically, American industry has risen to the task. For nearly a half-century, the U.S. military had access to an enormous and diverse domestic industrial base. Even when supplies ran low at the onset of the Korean War, a heavily industrialized America was able to ramp up within months to generate torrents of weapons that held off vastly larger Chinese forces for the next three years.

Today, however, U.S. domestic production capacity is a shriveled shadow of its former self. Crucial categories of industry for U.S. national defense are no longer built in any of the 50 states. With just 25 well-constructed attacks, using any of a variety of means, an adversarial military planner could cripple much of America’s manufacturing apparatus for producing advanced weapons.

Under the current U.S. government approach, industry cannot meet production demands to support allies under fire and deter war in the Pacific. Using case studies of munitions and shipbuilding production, this paper delineates the current state of affairs in the defense industrial base and provides pathways to mitigate, if not end, this strategic vulnerability.

THE NEW VECTOR FOR STRATEGIC COMPETITION: THE DEFENSE INDUSTRIAL BASE

Many American national security scholars have focused on the hightech innovation competition between the United States and China. This focus, however, risks losing sight of the defense industrial base—the thousands of companies of all sizes, types, and product lines—that turn those innovations into real-world weapons systems and platforms that win wars. Certainly, the contest for technological supremacy is crucial. But so is the contest for industrial production, relegated by some to be a 20th-century “legacy” function, at least until recently. New technologies need to be integrated with multiple existing weapons platforms and munitions to be effective. And they require materials, components, and microelectronics the United States is hard-pressed to acquire without ample foreign-supplied content, including materials and components from unreliable and unfriendly sources.

After elevating the innovation competition as the preeminent military challenge, many defense analysts move next to the readiness of the combat force: the number of aircraft prepared to fly, ships to sail, and infantry to deploy. Yet they also need to consider the readiness of the defense industrial base to mobilize production: how much and how quickly. U.S. leaders must thoroughly assess the capacity of the U.S. industrial enterprise, as compared to China, to produce the weapons and equipment most critical to an Indo-Pacific conflict.

The results will be sobering, if not alarming. In the last five years, Chinese firms have joined the ranks of the largest global defense companies at an accelerated pace.1 The country’s expanding exports of high-end systems—ranging from armed unmanned aerial vehicles to precision-guided munitions, submarines, and frigates—testify to China’s arrival on the global arms stage.2

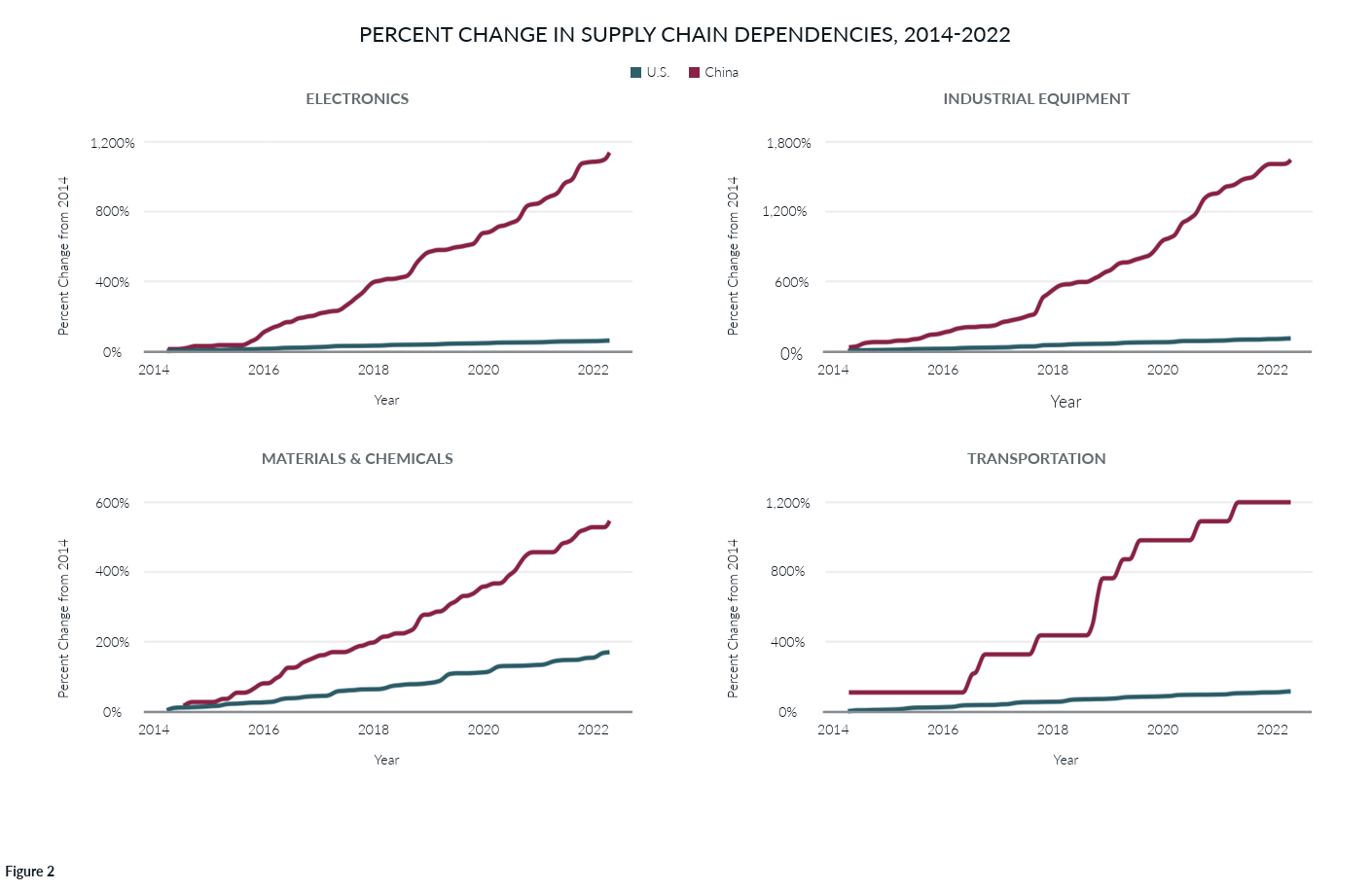

While China cranks out advanced weapons at a prodigious rate, it has also embedded itself in the supply chains for vital components of U.S. military platforms and weapons systems, creating U.S. reliance on the Chinese industrial base. Data from Govini’s Ark.ai, the software system for defense acquisition, shows that between 2005 and 2020, the level of Chinese suppliers in the U.S. supply chains quadrupled (Figure 1). In categories such as electronics, industrial equipment, and transportation, China’s expansion is even more pronounced. Between 2014 and 2022, U.S. dependence on China for electronics increased by 600% (Figure 2).

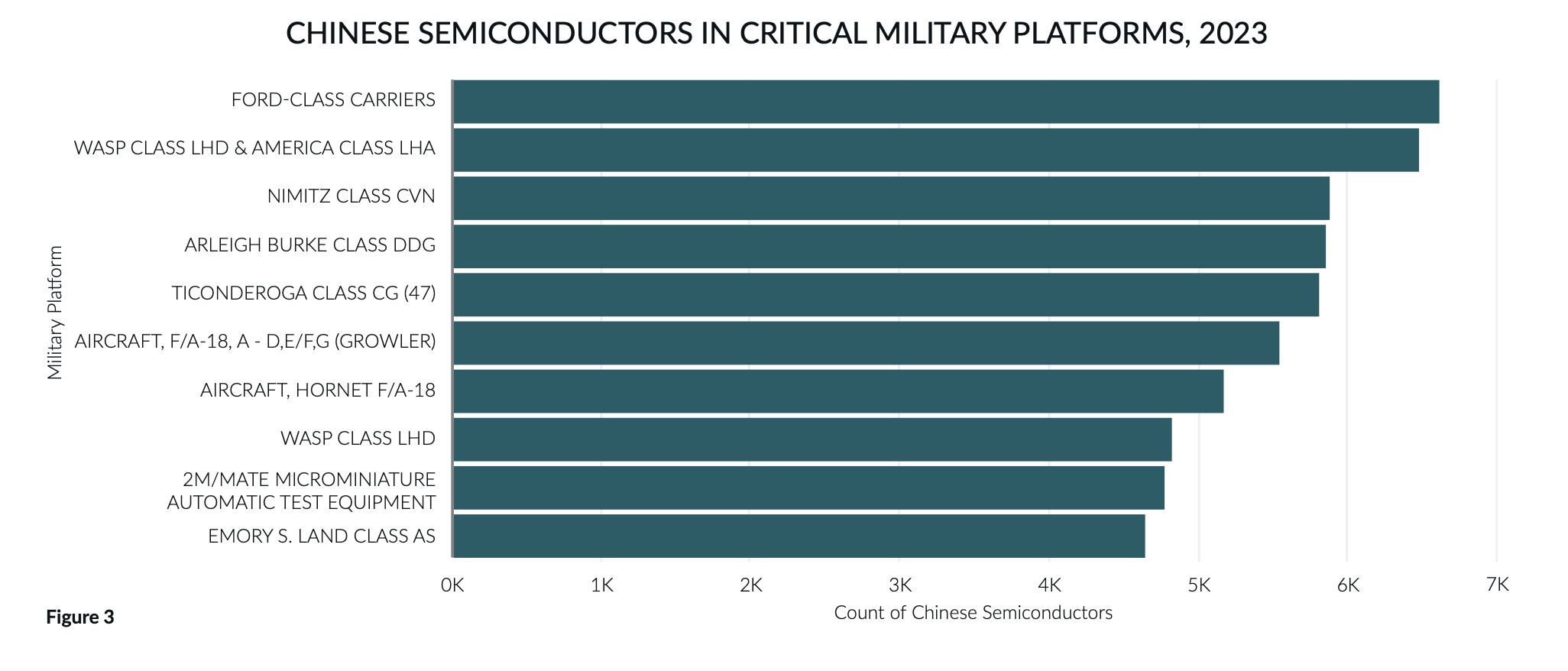

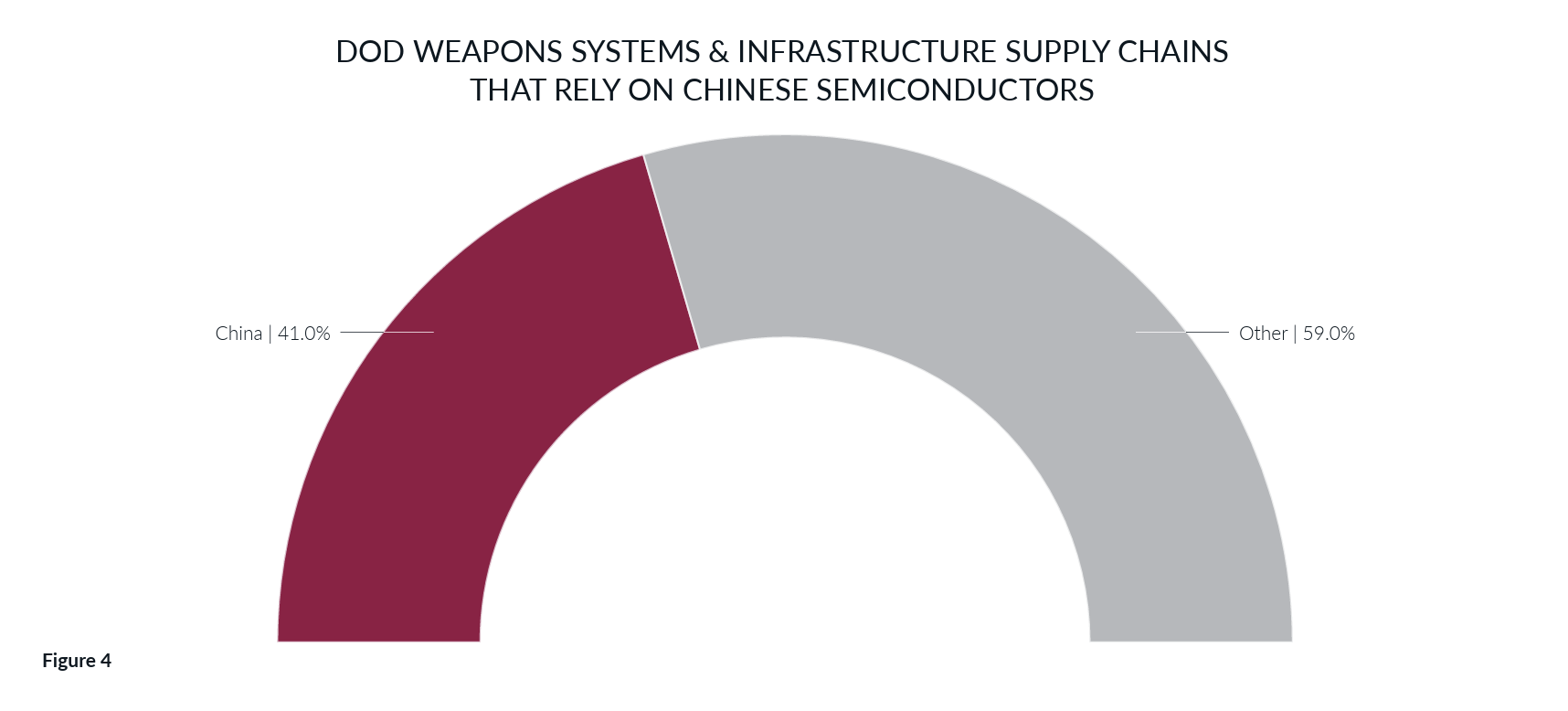

U.S. companies at the bottom of the supply chain pyramid often source these parts from China in open market transactions. As a result, many essential components in sensitive U.S. military systems now come from China. Countless major weapons platforms are vulnerable (Figure 3). Dependence on China for microelectronics, including semiconductors, packaging, and more, is particularly acute. Embedded in nearly every U.S. weapons system, semiconductors are foundational to U.S. military advantage. During a May 2023 visit to a Lockheed Martin missile factory in Alabama, President Joe Biden told employees that each Javelin anti-tank weapon produced there includes more than 200 semiconductors. Analysis from Ark.ai has found that more than 40% of the semiconductors that sustain DoD weapons systems and infrastructure depend on Chinese suppliers (Figure 4). Chinese semiconductor suppliers are inextricably linked to vital DoD weapons supply chains, such as the B-2 Bomber and Patriot air-defense missile (Figure 5).

THE PATH TO INDUSTRIAL FRAGILITY

How did we get into this predicament? When the Soviet Union collapsed and U.S. military spending shrank, America’s defense companies adjusted by merging and through adopting lean production and other financially driven “efficiencies.” That approach constituted the formula to remain in business. It did not deliver any savings in weapons costs, but instead resulted in a spike of spiraling per unit price increases. Moreover, with the decline in orders and the new business model, weapons stockpiles dwindled along with the production capacity to regenerate.3

As early as 2008, the Center for Strategic and Budgetary Assessments found that the migration toward “a low-volume, tailored-requirement production model” is incompatible with “an industrial surge capability that could turn out large numbers of weapons and systems should the need arise.” The costs for defense f irms to maintain excess production capacity have since increased, making it uneconomical under the current governmental acquisition system. Neither Congress nor the Defense Department has been willing to pay companies to maintain such capacity. Both branches of government embraced “just-in-time” inventory practices.4

Indeed, the U.S. government penalizes companies that might do otherwise. The Department of Defense generally pays only for contractor costs closely tied to the product numbers budgeted for the current program. That means the contract has little room to cover company expenses for maintaining facilities, manufacturing lines, parts warehouses, or relevant specialized technicians, engineers, or scientists needed in a contingency to surge production. The Pentagon’s “lowest price technically acceptable” ethos, i.e., spending not a penny more than is necessary to meet the most basic immediate requirements, has brought damaging secondary effects.

Military manufacturing cannot quickly be turned on and off at will. Once DoD orders decline, defense manufacturers necessarily close production lines or reduce them to veritable runts. These companies have few alternatives besides the United States and several other advanced allies to shop their defense-unique wares. A few mega-sized prime defense contractors sit atop a supply chain pyramid of tens of thousands of mid-to-small businesses. When the first tier curtails throughput, orders to smaller suppliers dry up. Some businesses may entirely close. In fact, many have left the defense industry over the last several decades–deciding to employ their limited time, talent, and capital in the larger and more lucrative commercial sector. Estimates indicate that the number of small to midsize contractors forming the bottom of the pyramid has shrunk from approximately 60,000 to 30,000 over recent decades.5

CASE STUDY: MUNITIONS EXPENDITURES

America’s struggles to scale munitions production after the Russian invasion of Ukraine starkly illustrate the brittleness of the U.S. industrial base. The Ukrainian military had a requirement to fire approximately 500 Javelin anti-tank missiles against Russian forces every day. In the first three months of the war, the United States shipped 7,000 Javelin missiles to Ukraine, around one-third of the American stockpile. The Lockheed Martin-Raytheon (now RTX) joint venture for the Javelin produced about 2,100 missiles a year.6 Congress has provided funds to double its production, but it will still take years to restock U.S. military inventories while continuing to support Ukraine.7

In addition, the Ukrainians have been shooting 6,000 to 7,000 field artillery rounds per day, and the Russians 40,000 to 50,000. At the onset of the conflict, U.S. production of 155 millimeter artillery rounds averaged 14,000 to 15,000 per month. With Congressional funding for additional production runs, the Defense Department expects monthly output to rise to 80,000, but not until 2025. In response to Ukrainian needs, the Army is also doubling the production of High Mobility Artillery Rocket System (HIMAR) rockets being expended.8

In the Pacific theater, ground-war capabilities like Javelins, artillery shells, and HIMAR rounds are not the prime weapons the United States will need to counter China. The distances to surmount are exponentially longer. The munitions the United States will require are of extended range: Long Range Anti-Ship Missiles (LRASMs), Joint Air-to-Surface Standoff Missiles (JASSMs), Naval Strike Missiles (NSMs), Tomahawk cruise missiles, and Harpoon anti-ship missiles. Ramping up the manufacture of these more complex, expensive, and currently low-volume systems will be a more difficult proposition than surging production to support the Ukrainian army.

The precise number of these longer-range munitions in U.S. military inventories is classified but known to be grossly inadequate relative to the China threat. After running two dozen wargame simulations, the Center for Strategic and International Studies concluded that the most essential American missile stocks would be gone in a week of combat in a Taiwan invasion scenario.9 Despite these shortfalls, the Fiscal Year 2023 defense procurement appropriation added fewer than 1,100 new mid-to-long range missiles: around 100 LRASMs, 660 JASSMs, 200 NSMs, and 100 Tomahawks.10 Dividing the total Congressional appropriation by the cost of each munition produces enough “long bolts” to support a few days of combat in the Pacific. To deter China, the United States likely requires months' worth.

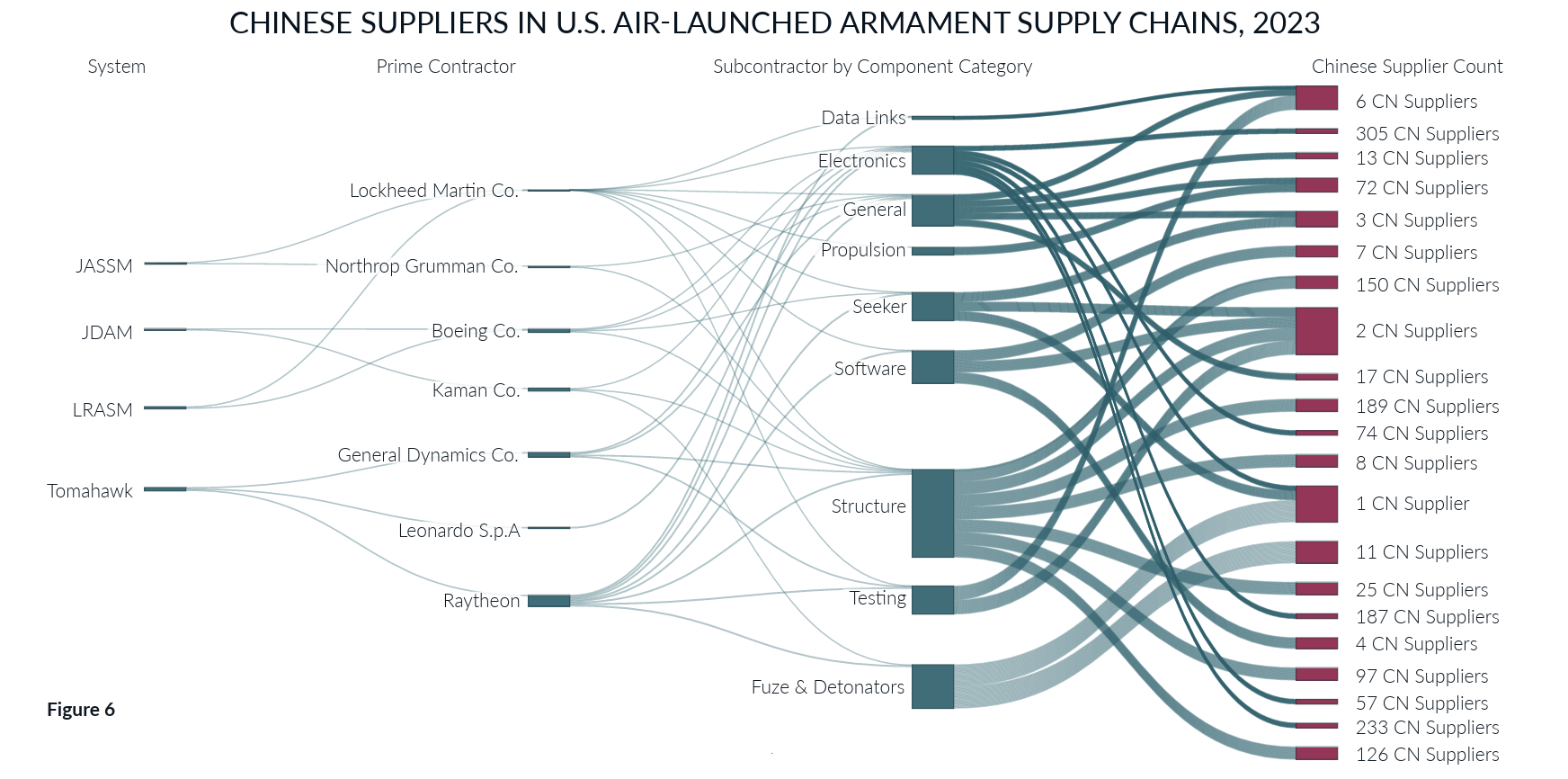

These long-range weapons are also vulnerable to the same supply chain challenges that plague the broader American industrial base. Adversarial influence is endemic to their production. Chinese companies are embedded in the supply chains of subcontractors to defense primes across system components such as electronics, software, fuses and detonators, and data links. Tracing these connections reveals an adversarial presence in critical long-range systems (Figure 6).

CASE STUDY: SHIPBUILDING & NAVAL READINESS

In any conflict scenario, China will vie with the United States for air, sea, and space superiority. The attrition of platforms and expenditure of munitions will be intense on both sides. China’s strategy is to cripple U.S. military nodes: naval and air facilities in Guam, Hawaii, and Japan, plus deployed aircraft carriers, destroyers, and cruisers. With current gaps in the industrial base that produces Navy ships, the United States will be hard-pressed to sustain operations in the theater.

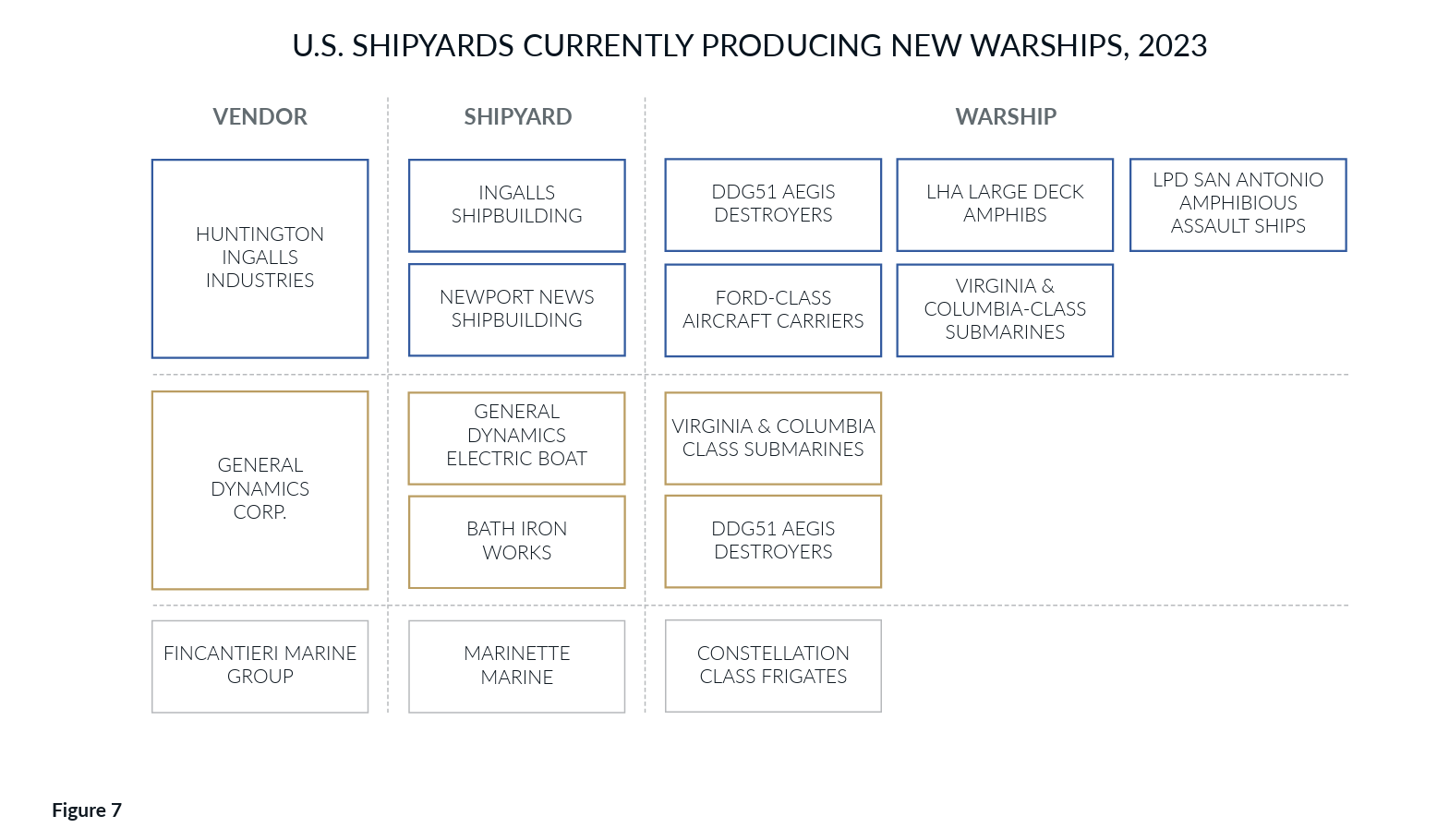

China has built a navy larger than that of the United States. China has fielded at least 340 new warships and is on track to reach 400 by 2025 and 440 by 2030.11 The U.S. Navy, by contrast, stands below 300 warships. While China’s larger fleet concentrates in the Indian and Pacific oceans, our smaller one is dispersed around the globe with numerous responsibilities and missions, including, most recently, the deployment of two full Carrier Strike Groups to deter Iranian threats to Israel during its Gaza operations. Additionally, China’s capacity to rebuild overwhelms that of the United States. America, once the world’s preeminent seafaring nation, is down to f ive shipyards capable of constructing new warships: aircraft carriers and small deck amphibs, destroyers and frigates, and missile and attack submarines (Figure 7).

Aside from these five Navy-specific yards, two other facilities build new major vessels important to U.S. security: Austal in Alabama constructs Coast Guard Heritage Class Cutters and NASSCO General Dynamics in California builds naval support ships: supply, tanker, logistics, prepositioning, sealift, and medical. Under current shifts, all seven of the yards operate near full capacity. Former Chief of Naval Operations Admiral Michael Gilday has stated that the entire U.S. defense industrial base cannot currently build three destroyers a year: it is “maxed out” at two or two and one-half per annum.12 China, in stark contrast, has 17 naval shipyards capable of new warship construction.13

Then there is the question of each nation’s overall shipbuilding base that can be mobilized in a conflict. China’s commercial shipbuilding capability dwarfs that of the United States. China and South Korea each account for over 35% of worldwide shipbuilding, followed by Japan at 16%. America has less than one-third of 1%.14

With current Navy plans and budgets, U.S. warship-builders do not see an economic case for creating more production capacity at their own expense. The United States government has been unwilling to fund the new shipyards. Nor has it yet considered the benefits of incentivizing experienced allied shipbuilders; for example, South Korea, Japan, and Italy could open yards in the United States, bringing their latest techniques and technology in the process.

CONCLUSION & RECOMMENDATIONS

The last enacted defense appropriation might have set a record at $853 billion, but absolute increases in warship construction and jet fighter funds were marginal; the funds for precision-guided munitions were low. The U.S. national defense requirement for such systems is an order of magnitude greater. It is vital now for the Department of Defense and federal government more broadly to address these challenges and leverage the resources at their disposal. Based on the data surrounding production capacity, supply chain resilience, and DoD spending, our recommendations are to:

1. Ramp up the purchases of critical arms and platforms. The U.S. capacity problem, whether it comes to building ships, aircraft, or precision strike, starts, first and foremost, with too few orders. One of the excuses for not ordering more is that the industrial base cannot meet the demand. This thinking is a self-defeating self-fulfilling prophecy. It is imperative that the United States starts ordering the equipment in the quantities needed to counter China. This requires the U.S. government to quintuple the purchases of mid-to-long-range conventional precision strike capabilities: the JAASM, LRASM, NSM, Advanced HARM, Tomahawk, and Harpoon. That will move U.S. stockpiles from around 800 to 3,200 missiles ordered per year.

There would be a one-time $3 billion investment for government paid facilities, equipment, and worker training and, then, $8 billion per year for the missiles ($1 billion buys approximately 400 of these weapons). In tandem, we should double the annual funding for surface warships and submarines. More long-range conventional strike munitions require additional air and sea platforms from which to fire.

2. Incentivize partnerships that facilitate innovation and cost reduction in major platforms. Let the DoD offer members of the new crop of small- and mid-sized businesses disrupting the aerospace and defense sector the opportunity to produce the mid to-extended range missiles we need, provided that they, as SpaceX did for space launch, can make them cheaper and faster. Hundreds of these companies have emerged with breathtaking abilities but limited access and familiarity with the ponderous defense budget process. New partnerships will bring innovation, per-unit cost reduction, and competition to an overly consolidated sector.

3. Give every DoD acquisition manager artificial intelligence enabled software platforms to run defense programs. Commercially available capabilities that offer immediate access to valuable external datasets are an essential part of operations for viable commercial manufacturing companies. Why DoD wouldn’t adopt similar, existing technology should baffle the mind of the taxpayer and warfighter alike. Purpose-built defense acquisition software capabilities allow DoD program managers and acquisition professionals to understand complex supply chain networks, uncover potential obstacles and solutions, and determine the most rapid production paths and opportunities to field new technologies rapidly.

4. Form a $10 billion fund to acquire critical components required for extended conventional strike, shipbuilding, and advanced jets. Stockpile sub-assemblies and parts, scarce materials, and machine tools as we did during the Cold War. The military services should inventory DoD boneyards to identify what systems could be rapidly reconfigured for combat use with some advanced preparation. Note that China is a prolific stockpiler of what it needs that is made in the United States. China scours the world and buys many years' worth of such items (advanced node semiconductors are the most notorious example). We would be shrewd to employ the same strategy where our weapons production supply chain has Chinese dependencies. If we cannot reshore or friend-shore a supply chain from China immediately, then should we build hedges now to reduce our vulnerabilities in case of a trade interruption or war.

5. Create a Defense Intelligence Agency open-source office to detail China’s entire domestic defense industrial base. A similar effort occurred when the U.S. faced the U.S.S.R. It is vital for us to know the specifics of the Chinese economic Order Of Battle. We should understand the supply chains, factories, logistics centers, and the people who run each node and their networks. Putin wrecked more than 75 years worth of European peace. Hamas visited horror upon Israel. China grows ever more belligerent, ambitious, and volatile. The United States needs a mass of what the military calls “fires” and the ships and aircraft to deliver them. Then, the United States can dampen the temptations and thwart the global ambitions of our adversaries and would-be enemies.

--

Jeffrey Jeb Nadaner is the Senior Vice President of Government Relations at Govini. Previously, Dr. Nadaner served as Executive Vice President of SAFE, directing bipartisan initiatives to incentivize U.S. and allied nations’ use of high-technology supply chains for automobiles, semiconductors, critical minerals, and strategic materials; Deputy Assistant Secretary of Defense for Industrial Policy; Director of the USMC Krulak Center of Innovation; and Vice President of Engineering and Technology at Lockheed Martin. Yale University awarded him his Ph.D. with a focus on competitive strategy, the University of Pennsylvania his J.D., and Duke University his B.A.

Tara Murphy Dougherty is the CEO of Govini. She has held leadership positions across technology, government, and nonprofit sectors, including at Palantir Technologies, and she served as Chief of Staff for Global Strategic Affairs in the Office of the Secretary of Defense, among other senior roles. She holds a bachelor’s from Georgia Tech and a master’s from Georgetown University. She serves on the Board of Directors for the National Defense Industrial Association and the National Defense University Foundation, and the Board of Advisors of the Reagan Institute’s National Security Innovation Base Program.

An extended variation of this essay by Jeb Nadaner will appear in 2024 in Confronting China, edited by Dr. James H. Anderson and Dr. Daniel Green, and published by ABC-CLIO.

ENDNOTES

1. Defense News, "Top 100 of 2023," Defense News, https://people.defensenews.com/top-100/. Accessed December 19, 2023.

2. Congressional Research Service, "China’s Military: The People’s Liberation Army (PLA)," p. 50, https://crsreports.congress.gov/ product/pdf/R/R46808. Accessed December 19, 2023.

3. John Paul Rathbone and Steff Chavez, "Military briefing: is the West running out of ammunition to supply Ukraine?," Financial Times, July 11, 2022, https://www.ft.com/content/d413576c-c4d5-4ca6-9050-58f3f8dc3c00 Accessed December 19, 2022.

4. Barry D. Watts, "The U.S. Industrial Base: Past, Present, Future," p. 73-75. Center for Strategic and Budgetary Assessments, https://csbaonline.org/uploads/documents/2008.10.15-Defense-Industrial-Base.pdf. Accessed December 19, 2023.

5. Chris Power, "Building Towards American Dynamism With Chris Power, CEO Of Hadrian," A16z Live, April 8th, 2022. https:// a16z-live.simplecast.com/episodes/building-towards-american-dynamism-hadrian-4VuPFYOa. Accessed December 19, 2023.

And: Joe Gould, “American exodus? 17,000 US defense suppliers may have left the defense sector [between 2011 and 2015],” Defense News, December 14, 2017, https://www.defensenews.com/breaking-news/2017/12/14/american-exodus-17000-us-defense-suppliersmay-have-left-the-defense-sector/. Accessed December 14, 2023.

And: CISA, “Defense Industrial Base,” https://www.cisa.gov/topics/critical-infrastructure-security-and-resilience/critical-infrastructuresectors/defense-industrial-base-sector. Accessed December 19, 2023.

And: U.S. Government Accountability Office (GAO), “Defense Industrial Base: DOD Should Take Actions to Strengthen Its Risk Mitigation Approach,” GAO-22-104154, https://www.gao.gov/products/gao-22-104154 , July 07, 2022. Accessed December 19, 2023.

6. Ben Fox, Aamer Madhani, Jay Reeves, "Push to arm Ukraine putting strain on US weapons stockpile," Military Times, May 3, 2022. https://www.militarytimes.com/news/your-military/2022/05/03/push-to-arm-ukraine-putting-strain-on-us-weapons-stockpile/. Accessed December 19, 2023.

7. Thomas Newdick,"Production Of In-Demand Javelin Missiles Set To Almost Double," The Drive, May 2, 2022. https://www. thedrive.com/the-war-zone/production-of-in-demand-javelin-missiles-set-to-almost-double. Accessed December 19, 2023

8. Joe Gould, "Army plans ‘dramatic’ ammo production boost as Ukraine drains stocks." Defense News, December 5, 2022. https://www.defensenews.com/pentagon/2022/12/05/army-plans-dramatic-ammo-production-boost-as-ukraine-drains-stocks/. Accessed December 19, 2023.

9. Mark F. Cancian, Matthew Cancian, and Eric Heginbotham, “The First Battle of the Next War: Wargaming a Chinese Invasion of Taiwan–Wargaming a Chinese Invasion of Taiwan,” Center for Strategic and International Studies, January 2023, https://csis-websiteprod.s3.amazonaws.com/s3fs-public/publication/230109_Cancian_FirstBattle_NextWar.pdf?VersionId=WdEUwJYWIySMPIr3ivhFolxC_ gZQuSOQ. Accessed December 19, 2023.

10. U.S. Senate Appropriations Committee, "DIVISION C - DEPARTMENT OF DEFENSE APPROPRIATIONS ACT, 2023." https:// www.appropriations.senate.gov/imo/media/doc/Division%20C%20-%20Defense. Accessed January 30, 2023.gZQuSOQ. Accessed December 19, 2023

11. Congressional Research Service, “Navy Force Structure and Shipbuilding Plans: Background and Issues for Congress,” November 16, 2023, https://crsreports.congress.gov/product/pdf/RL/RL32665/398. Accessed December 18, 2023.

12. Department of the Navy. CNO Participates in Reagan National Defense Forum Panel, December 3, 2022, https://www.navy. mil/DesktopModules/ArticleCS/Print.aspx?PortalId=1&ModuleId=590&Article=3238175. Accessed December 19, 2023.

And: Congressional Research Service, "Navy Force Structure and Shipbuilding Plans: Background and Issues for Congress," December 21, 2022, page 65, https://sgp.fas.org/crs/weapons/RL32665.pdf. Accessed December 19, 2023.

And: Rich Abbot, "CNO: Industry Cannot Build Three Destroyers Per Year Yet," Defense Daily, September 14, 2022, https://www. defensedaily.com/cno-industry-cannot-build-three-destroyers-per-year-yet/navy-usmc/. Accessed December 19, 2023.

13. Shreya Mundhra, "China Racing Ahead Of US Navy At Breakneck Speed; Building 20 Warships Per Year In 17 Shipyards–Top Official," EurAsian Times Desk, November 4, 2021, https://www.eurasiantimes.com/chinas-pla-navy-us-navy-a-breakneck-20-warships-peryear/#google_vignette. Accessed December 19, 2023.

14. MarketWatch, “Shipbuilding Market Size Related To Time And Cost Is Expected To Grow The Industry In Upcoming Years To 2026,” MarketWatch, January 26, 2023, https://www.marketwatch.com/press-release/shipbuilding-market-size-related-to-time-and-cost-isexpected-to-grow-the-industry-in-upcoming-years-to-2026-2023-01-26 Accessed January 29, 2023.

And: Mordor Intelligence, Shipbuilding Market - Growth, Trends, Covid-19 Impact, And Forecasts (2023 - 2028), https://www. mordorintelligence.com/industry-reports/ship-building-market. Accessed December 19, 2023.

And: Brandon Gaille, “34 Shipbuilding Industry Statistics, Trends & Analysis,” October 28, 2018, https://brandongaille.com/34-shipbuildingindustry-statistics-trends-analysis/. Accessed December 19, 2023.

And: Elizabeth Brotherton-Bunch, “New Legislation Aims to Revive America’s Shockingly Small Shipbuilding Industry,” Alliance for American Manufacturing, July 23, 2019, https://www.americanmanufacturing.org/blog/new-legislation-aims-to-revive-americas-shockingly-smallshipbuilding-industry/. Accessed December 19, 2023.

And: Alexander Wooley, “Float, Move, and Fight: How the U.S. Navy lost the shipbuilding race,” Foreign Policy, October 10, 2021, https:// foreignpolicy.com/2021/10/10/us-navy-shipbuilding-sea-power-failure-decline-competition-china/. Accessed December 19, 2023.

And: “Final Report Shipbuilding,” Spring 2015, NDU Eisenhower School, https://es.ndu.edu/Portals/75/Documents/industry-study/ reports/2015/es-is-report-shipbuilding-2015.pdf. Accessed December 19, 2023.

INTRODUCTION

In conflict, the ability to sustain the demands of combat over the long haul separates the victorious from the vanquished. To triumph, a nation requires ample weapons and stores and the capacity quickly to produce more. If that capacity and capability are uncertain, its deterrence abilities are weak. Aggression becomes appealing to its enemies.

What is the current state of production capacity across America’s industrial base, compared to adversaries such as the People’s Republic of China, which the U.S. military calls our principal pacing threat? The conflict in Ukraine has illuminated inadequate numbers of weapons in the U.S. inventory, from artillery shells to anti-aircraft missiles, due to an undersized workshop for war, a predicament the unexpected necessity to backstop Israel after the October attacks exacerbated. Overall, U.S. military systems are too old and few. Its magazine stocks are too low.

The United States will need a magnitude more of the weapons systems and production capacity to deter war in the Pacific and prevail if necessary. China’s leaders will only be deterred if they know the United States can sustain protracted conflict for months to come: destroying the People’s Liberation Army’s ships and satellites; devastating their naval, air, and missile formations; and choking off their pivotal supply chains.

Historically, American industry has risen to the task. For nearly a half-century, the U.S. military had access to an enormous and diverse domestic industrial base. Even when supplies ran low at the onset of the Korean War, a heavily industrialized America was able to ramp up within months to generate torrents of weapons that held off vastly larger Chinese forces for the next three years.

Today, however, U.S. domestic production capacity is a shriveled shadow of its former self. Crucial categories of industry for U.S. national defense are no longer built in any of the 50 states. With just 25 well-constructed attacks, using any of a variety of means, an adversarial military planner could cripple much of America’s manufacturing apparatus for producing advanced weapons.

Under the current U.S. government approach, industry cannot meet production demands to support allies under fire and deter war in the Pacific. Using case studies of munitions and shipbuilding production, this paper delineates the current state of affairs in the defense industrial base and provides pathways to mitigate, if not end, this strategic vulnerability.

THE NEW VECTOR FOR STRATEGIC COMPETITION: THE DEFENSE INDUSTRIAL BASE

Many American national security scholars have focused on the hightech innovation competition between the United States and China. This focus, however, risks losing sight of the defense industrial base—the thousands of companies of all sizes, types, and product lines—that turn those innovations into real-world weapons systems and platforms that win wars. Certainly, the contest for technological supremacy is crucial. But so is the contest for industrial production, relegated by some to be a 20th-century “legacy” function, at least until recently. New technologies need to be integrated with multiple existing weapons platforms and munitions to be effective. And they require materials, components, and microelectronics the United States is hard-pressed to acquire without ample foreign-supplied content, including materials and components from unreliable and unfriendly sources.

After elevating the innovation competition as the preeminent military challenge, many defense analysts move next to the readiness of the combat force: the number of aircraft prepared to fly, ships to sail, and infantry to deploy. Yet they also need to consider the readiness of the defense industrial base to mobilize production: how much and how quickly. U.S. leaders must thoroughly assess the capacity of the U.S. industrial enterprise, as compared to China, to produce the weapons and equipment most critical to an Indo-Pacific conflict.

The results will be sobering, if not alarming. In the last five years, Chinese firms have joined the ranks of the largest global defense companies at an accelerated pace.1 The country’s expanding exports of high-end systems—ranging from armed unmanned aerial vehicles to precision-guided munitions, submarines, and frigates—testify to China’s arrival on the global arms stage.2

While China cranks out advanced weapons at a prodigious rate, it has also embedded itself in the supply chains for vital components of U.S. military platforms and weapons systems, creating U.S. reliance on the Chinese industrial base. Data from Govini’s Ark.ai, the software system for defense acquisition, shows that between 2005 and 2020, the level of Chinese suppliers in the U.S. supply chains quadrupled (Figure 1). In categories such as electronics, industrial equipment, and transportation, China’s expansion is even more pronounced. Between 2014 and 2022, U.S. dependence on China for electronics increased by 600% (Figure 2).

U.S. companies at the bottom of the supply chain pyramid often source these parts from China in open market transactions. As a result, many essential components in sensitive U.S. military systems now come from China. Countless major weapons platforms are vulnerable (Figure 3). Dependence on China for microelectronics, including semiconductors, packaging, and more, is particularly acute. Embedded in nearly every U.S. weapons system, semiconductors are foundational to U.S. military advantage. During a May 2023 visit to a Lockheed Martin missile factory in Alabama, President Joe Biden told employees that each Javelin anti-tank weapon produced there includes more than 200 semiconductors. Analysis from Ark.ai has found that more than 40% of the semiconductors that sustain DoD weapons systems and infrastructure depend on Chinese suppliers (Figure 4). Chinese semiconductor suppliers are inextricably linked to vital DoD weapons supply chains, such as the B-2 Bomber and Patriot air-defense missile (Figure 5).

THE PATH TO INDUSTRIAL FRAGILITY

How did we get into this predicament? When the Soviet Union collapsed and U.S. military spending shrank, America’s defense companies adjusted by merging and through adopting lean production and other financially driven “efficiencies.” That approach constituted the formula to remain in business. It did not deliver any savings in weapons costs, but instead resulted in a spike of spiraling per unit price increases. Moreover, with the decline in orders and the new business model, weapons stockpiles dwindled along with the production capacity to regenerate.3

As early as 2008, the Center for Strategic and Budgetary Assessments found that the migration toward “a low-volume, tailored-requirement production model” is incompatible with “an industrial surge capability that could turn out large numbers of weapons and systems should the need arise.” The costs for defense f irms to maintain excess production capacity have since increased, making it uneconomical under the current governmental acquisition system. Neither Congress nor the Defense Department has been willing to pay companies to maintain such capacity. Both branches of government embraced “just-in-time” inventory practices.4

Indeed, the U.S. government penalizes companies that might do otherwise. The Department of Defense generally pays only for contractor costs closely tied to the product numbers budgeted for the current program. That means the contract has little room to cover company expenses for maintaining facilities, manufacturing lines, parts warehouses, or relevant specialized technicians, engineers, or scientists needed in a contingency to surge production. The Pentagon’s “lowest price technically acceptable” ethos, i.e., spending not a penny more than is necessary to meet the most basic immediate requirements, has brought damaging secondary effects.

Military manufacturing cannot quickly be turned on and off at will. Once DoD orders decline, defense manufacturers necessarily close production lines or reduce them to veritable runts. These companies have few alternatives besides the United States and several other advanced allies to shop their defense-unique wares. A few mega-sized prime defense contractors sit atop a supply chain pyramid of tens of thousands of mid-to-small businesses. When the first tier curtails throughput, orders to smaller suppliers dry up. Some businesses may entirely close. In fact, many have left the defense industry over the last several decades–deciding to employ their limited time, talent, and capital in the larger and more lucrative commercial sector. Estimates indicate that the number of small to midsize contractors forming the bottom of the pyramid has shrunk from approximately 60,000 to 30,000 over recent decades.5

CASE STUDY: MUNITIONS EXPENDITURES

America’s struggles to scale munitions production after the Russian invasion of Ukraine starkly illustrate the brittleness of the U.S. industrial base. The Ukrainian military had a requirement to fire approximately 500 Javelin anti-tank missiles against Russian forces every day. In the first three months of the war, the United States shipped 7,000 Javelin missiles to Ukraine, around one-third of the American stockpile. The Lockheed Martin-Raytheon (now RTX) joint venture for the Javelin produced about 2,100 missiles a year.6 Congress has provided funds to double its production, but it will still take years to restock U.S. military inventories while continuing to support Ukraine.7

In addition, the Ukrainians have been shooting 6,000 to 7,000 field artillery rounds per day, and the Russians 40,000 to 50,000. At the onset of the conflict, U.S. production of 155 millimeter artillery rounds averaged 14,000 to 15,000 per month. With Congressional funding for additional production runs, the Defense Department expects monthly output to rise to 80,000, but not until 2025. In response to Ukrainian needs, the Army is also doubling the production of High Mobility Artillery Rocket System (HIMAR) rockets being expended.8

In the Pacific theater, ground-war capabilities like Javelins, artillery shells, and HIMAR rounds are not the prime weapons the United States will need to counter China. The distances to surmount are exponentially longer. The munitions the United States will require are of extended range: Long Range Anti-Ship Missiles (LRASMs), Joint Air-to-Surface Standoff Missiles (JASSMs), Naval Strike Missiles (NSMs), Tomahawk cruise missiles, and Harpoon anti-ship missiles. Ramping up the manufacture of these more complex, expensive, and currently low-volume systems will be a more difficult proposition than surging production to support the Ukrainian army.

The precise number of these longer-range munitions in U.S. military inventories is classified but known to be grossly inadequate relative to the China threat. After running two dozen wargame simulations, the Center for Strategic and International Studies concluded that the most essential American missile stocks would be gone in a week of combat in a Taiwan invasion scenario.9 Despite these shortfalls, the Fiscal Year 2023 defense procurement appropriation added fewer than 1,100 new mid-to-long range missiles: around 100 LRASMs, 660 JASSMs, 200 NSMs, and 100 Tomahawks.10 Dividing the total Congressional appropriation by the cost of each munition produces enough “long bolts” to support a few days of combat in the Pacific. To deter China, the United States likely requires months' worth.

These long-range weapons are also vulnerable to the same supply chain challenges that plague the broader American industrial base. Adversarial influence is endemic to their production. Chinese companies are embedded in the supply chains of subcontractors to defense primes across system components such as electronics, software, fuses and detonators, and data links. Tracing these connections reveals an adversarial presence in critical long-range systems (Figure 6).

CASE STUDY: SHIPBUILDING & NAVAL READINESS

In any conflict scenario, China will vie with the United States for air, sea, and space superiority. The attrition of platforms and expenditure of munitions will be intense on both sides. China’s strategy is to cripple U.S. military nodes: naval and air facilities in Guam, Hawaii, and Japan, plus deployed aircraft carriers, destroyers, and cruisers. With current gaps in the industrial base that produces Navy ships, the United States will be hard-pressed to sustain operations in the theater.

China has built a navy larger than that of the United States. China has fielded at least 340 new warships and is on track to reach 400 by 2025 and 440 by 2030.11 The U.S. Navy, by contrast, stands below 300 warships. While China’s larger fleet concentrates in the Indian and Pacific oceans, our smaller one is dispersed around the globe with numerous responsibilities and missions, including, most recently, the deployment of two full Carrier Strike Groups to deter Iranian threats to Israel during its Gaza operations. Additionally, China’s capacity to rebuild overwhelms that of the United States. America, once the world’s preeminent seafaring nation, is down to f ive shipyards capable of constructing new warships: aircraft carriers and small deck amphibs, destroyers and frigates, and missile and attack submarines (Figure 7).

Aside from these five Navy-specific yards, two other facilities build new major vessels important to U.S. security: Austal in Alabama constructs Coast Guard Heritage Class Cutters and NASSCO General Dynamics in California builds naval support ships: supply, tanker, logistics, prepositioning, sealift, and medical. Under current shifts, all seven of the yards operate near full capacity. Former Chief of Naval Operations Admiral Michael Gilday has stated that the entire U.S. defense industrial base cannot currently build three destroyers a year: it is “maxed out” at two or two and one-half per annum.12 China, in stark contrast, has 17 naval shipyards capable of new warship construction.13

Then there is the question of each nation’s overall shipbuilding base that can be mobilized in a conflict. China’s commercial shipbuilding capability dwarfs that of the United States. China and South Korea each account for over 35% of worldwide shipbuilding, followed by Japan at 16%. America has less than one-third of 1%.14

With current Navy plans and budgets, U.S. warship-builders do not see an economic case for creating more production capacity at their own expense. The United States government has been unwilling to fund the new shipyards. Nor has it yet considered the benefits of incentivizing experienced allied shipbuilders; for example, South Korea, Japan, and Italy could open yards in the United States, bringing their latest techniques and technology in the process.

CONCLUSION & RECOMMENDATIONS

The last enacted defense appropriation might have set a record at $853 billion, but absolute increases in warship construction and jet fighter funds were marginal; the funds for precision-guided munitions were low. The U.S. national defense requirement for such systems is an order of magnitude greater. It is vital now for the Department of Defense and federal government more broadly to address these challenges and leverage the resources at their disposal. Based on the data surrounding production capacity, supply chain resilience, and DoD spending, our recommendations are to:

1. Ramp up the purchases of critical arms and platforms. The U.S. capacity problem, whether it comes to building ships, aircraft, or precision strike, starts, first and foremost, with too few orders. One of the excuses for not ordering more is that the industrial base cannot meet the demand. This thinking is a self-defeating self-fulfilling prophecy. It is imperative that the United States starts ordering the equipment in the quantities needed to counter China. This requires the U.S. government to quintuple the purchases of mid-to-long-range conventional precision strike capabilities: the JAASM, LRASM, NSM, Advanced HARM, Tomahawk, and Harpoon. That will move U.S. stockpiles from around 800 to 3,200 missiles ordered per year.

There would be a one-time $3 billion investment for government paid facilities, equipment, and worker training and, then, $8 billion per year for the missiles ($1 billion buys approximately 400 of these weapons). In tandem, we should double the annual funding for surface warships and submarines. More long-range conventional strike munitions require additional air and sea platforms from which to fire.

2. Incentivize partnerships that facilitate innovation and cost reduction in major platforms. Let the DoD offer members of the new crop of small- and mid-sized businesses disrupting the aerospace and defense sector the opportunity to produce the mid to-extended range missiles we need, provided that they, as SpaceX did for space launch, can make them cheaper and faster. Hundreds of these companies have emerged with breathtaking abilities but limited access and familiarity with the ponderous defense budget process. New partnerships will bring innovation, per-unit cost reduction, and competition to an overly consolidated sector.

3. Give every DoD acquisition manager artificial intelligence enabled software platforms to run defense programs. Commercially available capabilities that offer immediate access to valuable external datasets are an essential part of operations for viable commercial manufacturing companies. Why DoD wouldn’t adopt similar, existing technology should baffle the mind of the taxpayer and warfighter alike. Purpose-built defense acquisition software capabilities allow DoD program managers and acquisition professionals to understand complex supply chain networks, uncover potential obstacles and solutions, and determine the most rapid production paths and opportunities to field new technologies rapidly.

4. Form a $10 billion fund to acquire critical components required for extended conventional strike, shipbuilding, and advanced jets. Stockpile sub-assemblies and parts, scarce materials, and machine tools as we did during the Cold War. The military services should inventory DoD boneyards to identify what systems could be rapidly reconfigured for combat use with some advanced preparation. Note that China is a prolific stockpiler of what it needs that is made in the United States. China scours the world and buys many years' worth of such items (advanced node semiconductors are the most notorious example). We would be shrewd to employ the same strategy where our weapons production supply chain has Chinese dependencies. If we cannot reshore or friend-shore a supply chain from China immediately, then should we build hedges now to reduce our vulnerabilities in case of a trade interruption or war.

5. Create a Defense Intelligence Agency open-source office to detail China’s entire domestic defense industrial base. A similar effort occurred when the U.S. faced the U.S.S.R. It is vital for us to know the specifics of the Chinese economic Order Of Battle. We should understand the supply chains, factories, logistics centers, and the people who run each node and their networks. Putin wrecked more than 75 years worth of European peace. Hamas visited horror upon Israel. China grows ever more belligerent, ambitious, and volatile. The United States needs a mass of what the military calls “fires” and the ships and aircraft to deliver them. Then, the United States can dampen the temptations and thwart the global ambitions of our adversaries and would-be enemies.

--

Jeffrey Jeb Nadaner is the Senior Vice President of Government Relations at Govini. Previously, Dr. Nadaner served as Executive Vice President of SAFE, directing bipartisan initiatives to incentivize U.S. and allied nations’ use of high-technology supply chains for automobiles, semiconductors, critical minerals, and strategic materials; Deputy Assistant Secretary of Defense for Industrial Policy; Director of the USMC Krulak Center of Innovation; and Vice President of Engineering and Technology at Lockheed Martin. Yale University awarded him his Ph.D. with a focus on competitive strategy, the University of Pennsylvania his J.D., and Duke University his B.A.

Tara Murphy Dougherty is the CEO of Govini. She has held leadership positions across technology, government, and nonprofit sectors, including at Palantir Technologies, and she served as Chief of Staff for Global Strategic Affairs in the Office of the Secretary of Defense, among other senior roles. She holds a bachelor’s from Georgia Tech and a master’s from Georgetown University. She serves on the Board of Directors for the National Defense Industrial Association and the National Defense University Foundation, and the Board of Advisors of the Reagan Institute’s National Security Innovation Base Program.

An extended variation of this essay by Jeb Nadaner will appear in 2024 in Confronting China, edited by Dr. James H. Anderson and Dr. Daniel Green, and published by ABC-CLIO.

ENDNOTES

1. Defense News, "Top 100 of 2023," Defense News, https://people.defensenews.com/top-100/. Accessed December 19, 2023.

2. Congressional Research Service, "China’s Military: The People’s Liberation Army (PLA)," p. 50, https://crsreports.congress.gov/ product/pdf/R/R46808. Accessed December 19, 2023.

3. John Paul Rathbone and Steff Chavez, "Military briefing: is the West running out of ammunition to supply Ukraine?," Financial Times, July 11, 2022, https://www.ft.com/content/d413576c-c4d5-4ca6-9050-58f3f8dc3c00 Accessed December 19, 2022.

4. Barry D. Watts, "The U.S. Industrial Base: Past, Present, Future," p. 73-75. Center for Strategic and Budgetary Assessments, https://csbaonline.org/uploads/documents/2008.10.15-Defense-Industrial-Base.pdf. Accessed December 19, 2023.

5. Chris Power, "Building Towards American Dynamism With Chris Power, CEO Of Hadrian," A16z Live, April 8th, 2022. https:// a16z-live.simplecast.com/episodes/building-towards-american-dynamism-hadrian-4VuPFYOa. Accessed December 19, 2023.

And: Joe Gould, “American exodus? 17,000 US defense suppliers may have left the defense sector [between 2011 and 2015],” Defense News, December 14, 2017, https://www.defensenews.com/breaking-news/2017/12/14/american-exodus-17000-us-defense-suppliersmay-have-left-the-defense-sector/. Accessed December 14, 2023.

And: CISA, “Defense Industrial Base,” https://www.cisa.gov/topics/critical-infrastructure-security-and-resilience/critical-infrastructuresectors/defense-industrial-base-sector. Accessed December 19, 2023.

And: U.S. Government Accountability Office (GAO), “Defense Industrial Base: DOD Should Take Actions to Strengthen Its Risk Mitigation Approach,” GAO-22-104154, https://www.gao.gov/products/gao-22-104154 , July 07, 2022. Accessed December 19, 2023.

6. Ben Fox, Aamer Madhani, Jay Reeves, "Push to arm Ukraine putting strain on US weapons stockpile," Military Times, May 3, 2022. https://www.militarytimes.com/news/your-military/2022/05/03/push-to-arm-ukraine-putting-strain-on-us-weapons-stockpile/. Accessed December 19, 2023.

7. Thomas Newdick,"Production Of In-Demand Javelin Missiles Set To Almost Double," The Drive, May 2, 2022. https://www. thedrive.com/the-war-zone/production-of-in-demand-javelin-missiles-set-to-almost-double. Accessed December 19, 2023

8. Joe Gould, "Army plans ‘dramatic’ ammo production boost as Ukraine drains stocks." Defense News, December 5, 2022. https://www.defensenews.com/pentagon/2022/12/05/army-plans-dramatic-ammo-production-boost-as-ukraine-drains-stocks/. Accessed December 19, 2023.

9. Mark F. Cancian, Matthew Cancian, and Eric Heginbotham, “The First Battle of the Next War: Wargaming a Chinese Invasion of Taiwan–Wargaming a Chinese Invasion of Taiwan,” Center for Strategic and International Studies, January 2023, https://csis-websiteprod.s3.amazonaws.com/s3fs-public/publication/230109_Cancian_FirstBattle_NextWar.pdf?VersionId=WdEUwJYWIySMPIr3ivhFolxC_ gZQuSOQ. Accessed December 19, 2023.

10. U.S. Senate Appropriations Committee, "DIVISION C - DEPARTMENT OF DEFENSE APPROPRIATIONS ACT, 2023." https:// www.appropriations.senate.gov/imo/media/doc/Division%20C%20-%20Defense. Accessed January 30, 2023.gZQuSOQ. Accessed December 19, 2023

11. Congressional Research Service, “Navy Force Structure and Shipbuilding Plans: Background and Issues for Congress,” November 16, 2023, https://crsreports.congress.gov/product/pdf/RL/RL32665/398. Accessed December 18, 2023.

12. Department of the Navy. CNO Participates in Reagan National Defense Forum Panel, December 3, 2022, https://www.navy. mil/DesktopModules/ArticleCS/Print.aspx?PortalId=1&ModuleId=590&Article=3238175. Accessed December 19, 2023.

And: Congressional Research Service, "Navy Force Structure and Shipbuilding Plans: Background and Issues for Congress," December 21, 2022, page 65, https://sgp.fas.org/crs/weapons/RL32665.pdf. Accessed December 19, 2023.

And: Rich Abbot, "CNO: Industry Cannot Build Three Destroyers Per Year Yet," Defense Daily, September 14, 2022, https://www. defensedaily.com/cno-industry-cannot-build-three-destroyers-per-year-yet/navy-usmc/. Accessed December 19, 2023.

13. Shreya Mundhra, "China Racing Ahead Of US Navy At Breakneck Speed; Building 20 Warships Per Year In 17 Shipyards–Top Official," EurAsian Times Desk, November 4, 2021, https://www.eurasiantimes.com/chinas-pla-navy-us-navy-a-breakneck-20-warships-peryear/#google_vignette. Accessed December 19, 2023.

14. MarketWatch, “Shipbuilding Market Size Related To Time And Cost Is Expected To Grow The Industry In Upcoming Years To 2026,” MarketWatch, January 26, 2023, https://www.marketwatch.com/press-release/shipbuilding-market-size-related-to-time-and-cost-isexpected-to-grow-the-industry-in-upcoming-years-to-2026-2023-01-26 Accessed January 29, 2023.

And: Mordor Intelligence, Shipbuilding Market - Growth, Trends, Covid-19 Impact, And Forecasts (2023 - 2028), https://www. mordorintelligence.com/industry-reports/ship-building-market. Accessed December 19, 2023.

And: Brandon Gaille, “34 Shipbuilding Industry Statistics, Trends & Analysis,” October 28, 2018, https://brandongaille.com/34-shipbuildingindustry-statistics-trends-analysis/. Accessed December 19, 2023.

And: Elizabeth Brotherton-Bunch, “New Legislation Aims to Revive America’s Shockingly Small Shipbuilding Industry,” Alliance for American Manufacturing, July 23, 2019, https://www.americanmanufacturing.org/blog/new-legislation-aims-to-revive-americas-shockingly-smallshipbuilding-industry/. Accessed December 19, 2023.

And: Alexander Wooley, “Float, Move, and Fight: How the U.S. Navy lost the shipbuilding race,” Foreign Policy, October 10, 2021, https:// foreignpolicy.com/2021/10/10/us-navy-shipbuilding-sea-power-failure-decline-competition-china/. Accessed December 19, 2023.

And: “Final Report Shipbuilding,” Spring 2015, NDU Eisenhower School, https://es.ndu.edu/Portals/75/Documents/industry-study/ reports/2015/es-is-report-shipbuilding-2015.pdf. Accessed December 19, 2023.