From raw minerals to advanced weapon systems—from rock to rocket—there lies a reality: America’s military superiority increasingly depends on China. China recently tightened its grip on critical minerals essential to defense and commercial technologies by expanding its export controls to include tungsten, tellurium, and other vital materials. This action builds upon earlier restrictions introduced in 2024, targeting gallium, germanium, and antimony.

China recently tightened its grip on critical minerals essential to defense and commercial technologies by expanding its export controls to include tungsten, tellurium, and other vital materials. This action builds upon earlier restrictions introduced in 2024, targeting gallium, germanium, and antimony.

Though these minerals rarely capture national attention, they underpin crucial components of America’s defense infrastructure. They are integral to radar systems that detect threats, night-vision equipment that provides tactical advantages, and precision-guided munitions essential to modern warfare. America’s heavy reliance on Chinese suppliers for these strategic resources poses a major national security risk.

Importance of These Critical Minerals

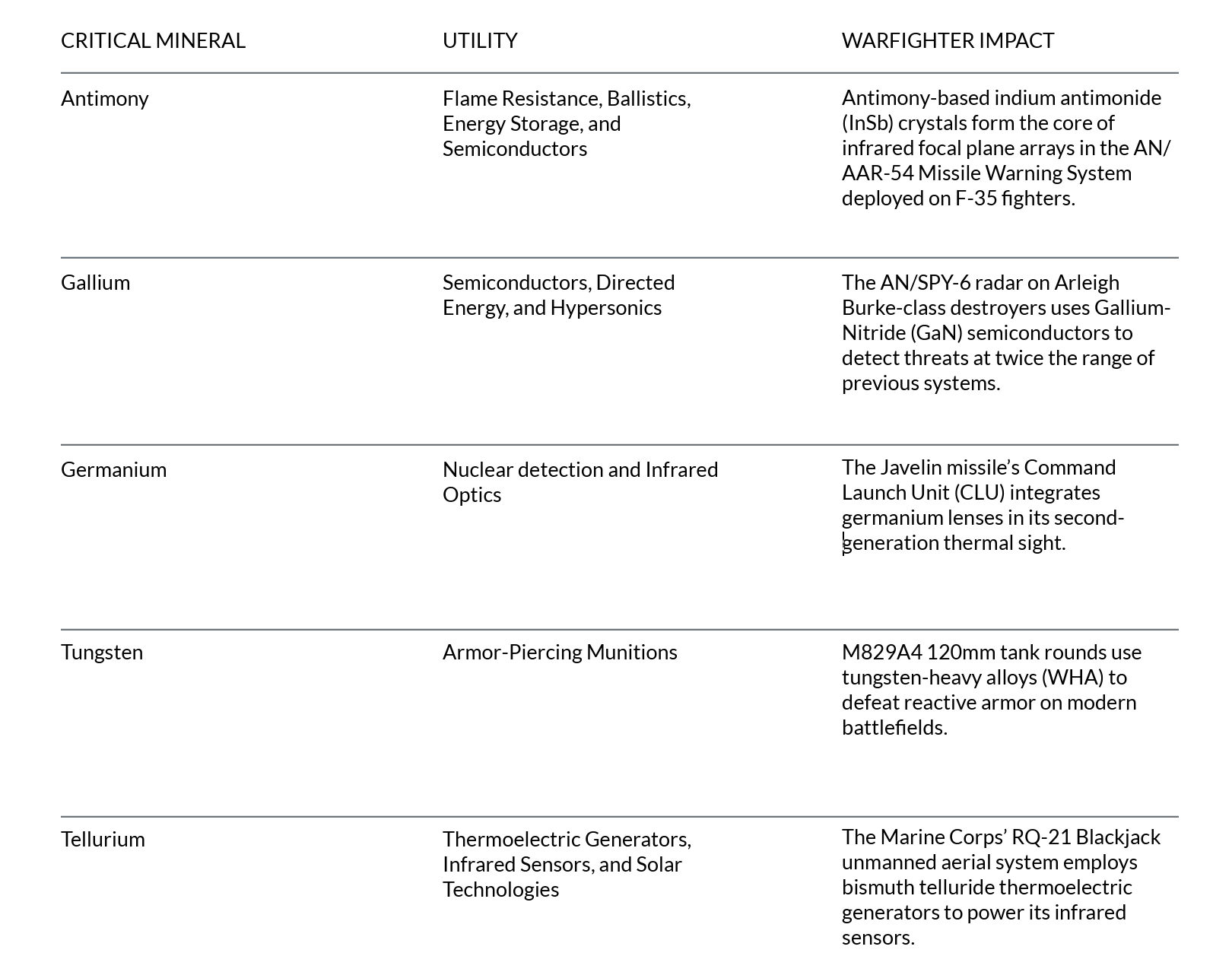

Antimony, gallium, germanium, tungsten, and tellurium each play specialized roles in military applications, ranging from flameresistant gear and advanced semiconductors to nuclear detection and hypersonic weaponry. These materials are indispensable for modern defense infrastructure, yet their supply chains remain vulnerable to geopolitical risks. The below examples underscore how these elements underpin foundational military capabilities.

The export bans and controls come as DoD increases its demand for parts containing critical minerals to support the acquisition lifecycle of weapon systems. Since 2010, Department of Defense (DoD) contracts for components containing these five critical minerals have increased by an average of 23.2% per year (Figure 1) while the DoD’s spending on these components has grown by about 7% annually. The increases are larger within specific critical minerals —contracts for parts with gallium have surged by 41.8% each year, and spending on germanium-containing parts has risen by 16.1% year-over-year (Figure 2).

This upward trend of spending also reflects broader reliance on these minerals. More than 80,000 parts across 1,900 weapon systems incorporate antimony, gallium, germanium, tungsten, or tellurium, meaning nearly 78% of all DoD weapon systems are potentially affected. This dependence spans across the military services. Over 91% of Navy weapon systems rely on these materials, while 61.7% of Marine Corps systems rely on parts connected to these critical minerals (Figure 3). Some of the systems most impacted include the Arleigh Burke Class destroyers, America Class amphibious assault ships, Nimitz Class aircraft carriers, and the Minuteman III nuclear missile program.

The growing reliance on these critical minerals exacerbates concerns over supply chain stability and adversarial reliance.

The modernization of U.S. military capabilities and expanding operational demand is driving a significant increase in material consumption. But how does the U.S. secure these critical resources?

The journey—from extracting raw rock to deploying a fully assembled rocket— follows a complex network of suppliers, processors, and manufacturers that convert raw minerals into military-grade components. This process involves several key stages: mining the mineral, refining it, manufacturing the end product, and finally, distributing it to the Department of Defense. Every link in this chain must remain free from adversarial influence. For example, even if antimony is mined in Australia, if it is refined in China, the ban will prevent it from ever touching an American weapon system.

Over 43,000 different supply chains have some level of Chinese dependence extending down to six tiers of suppliers. This analysis identified all the potential ways that a mineral is refined, made into a part, and then procured by the Department of Defense to support the production of over 1,900 weapon systems. 88% of these supply chains are influenced by China and potentially jeopardized by the Chinese exit bans (Figure 4).

Let’s examine antimony’s role in four key weapon systems—the F-16 fighter jet, the Arleigh Burke-class destroyer, the Minuteman III missile, and the Wasp-class amphibious assault ship. Each platform represents decades of American innovation and meticulous engineering, and yet more than 80% of the antimony required for these systems is affected by the ban (Figure 5).

Most of the impact of the ban comes from China’s dominance in the mining sector, with roughly 60% of global antimony is mined in China.1 However, even if antimony is not mined in China, Chinese firms operate internationally to further entrench their mineral dominance. For example, Tibet Huayu, a subsidiary of China’s state-owned Tibet Mineral Development Co., operates the Anzob antimony-gold complex in Tajikistan through a $200 million joint venture with Tajik Aluminium Company (TALCO).2 Other countries with Chinese involvement in antimony mining are Russia3 and Ghana.4

China’s control over raw antimony processing, another step in the supply chain, further limits U.S. supply. Nearly one-third of antimony that was initially processed elsewhere ends up being refined in China. Combined with China’s extensive manufacturing capabilities, only 19% of the antimony needed for these weapon systems is available outside of China. This heavy reliance on Chinese-refined antimony not only exposes critical defense supply chains to potential political and economic leverage, but may also drive up costs and delay production timelines for U.S. military platforms.

We have already seen an impact on DoD procurement. In the three months following China’s export ban on antimony, gallium, and germanium, parts containing these critical minerals saw prices increase by an average of 5.2% after the ban, compared to procurements of those same parts the few months prior. More specifically, the price for components containing gallium increased by 6.0%, those with antimony by 4.5%, and germanium by 1.6%. All other parts increased by an average of only 1.4% (Figure 6).5

These figures not only reflect immediate market responses, but also signal the potential for more severe disruptions as the bans continue to influence global supply dynamics. As vendors begin to grapple with the indirect effects of these export restrictions, further price escalations are anticipated.

The data points to actionable solutions that can begin to address these strategic vulnerabilities.

Increase Domestic Capabilities

First, the United States must revive its domestic processing capabilities. Today, the United States exports raw precursors for more than 35 critical minerals to China to be processed before they are re-imported back. However, this cycle has been broken, as China now prevents exports of select critical minerals back to the United States. This dependency on foreign processing exposes our supply chains to geopolitical risk and undermines our economic sovereignty.

Addressing this challenge requires comprehensive mapping of material precursors and tax incentives that encourage private sector investment in domestic refining capabilities. While there has been progress—such as DoD investing $59.4 million under the Defense Production Act in February 2024 to support reserves in Idaho in an effort to boost domestic antimony production—there are still no domestic sources for gallium, germanium, or tungsten.

As an example, the United States has become a new producer of tellurium within the past three years. Working closely with the Department of Energy’s Critical Minerals Institute, private industry began extracting copper from the Kennecott mine in Utah, which has been instrumental in dropping the United States’ tellurium foreign reliance from 95% in 2019 down to 25% in 2023.6 The tellurium is refined in Canada then supplied to an American solar panel manufacturer. While we may not develop new domestic sources for every critical mineral, allied nations offer attractive augmentation of our supplies, from Australia antimony reserves to Canada’s refining capabilities.

Leverage Mineral Companionality

Material companionality is a critical yet overlooked factor shaping the viability of domestic mineral resources and national supply chain security. Pure critical minerals are rarely found in nature; instead, they usually appear alongside other materials in varying concentrations and smaller quantities. Consequently, sources of critical minerals exist within the United States and allied countries, yet these resources often remain unprocessed. Several factors contribute to this situation:

First, critical minerals within these mineral deposits frequently exist in low concentrations, requiring the processing of larger quantities of material to yield commercially viable amounts. This increased processing significantly raises operational costs, reducing profit margins and making extraction less economically appealing.

Second, extracting these metals from their associated minerals often necessitates advanced and costly extraction technologies. The substantial capital investments and high operating expenses required for such technologies can render domestic mineral processing economically unfeasible.

Finally, stringent licensing and permitting processes often hinder the extraction of companion minerals. Existing mining permits frequently authorize only the extraction of primary minerals, excluding secondary or companion minerals. Initiating extraction of additional minerals typically requires renewed regulatory discussions, extended governmental negotiations, and updated permits, further delaying production timelines.7

To address these challenges, the federal government should offer subsidies and contracts to incentivize companies to leverage mineral companionality. One example is the aforementioned effort in Idaho, where Perpetua Resources received up to $59 million under the Defense Production Act to redevelop an abandoned mining site. This funding specifically supports extracting antimony—a critical mineral previously overlooked due to its association with gold mining operations.8 Other efforts include the Netherlands-headquartered Nyrstar searching for government investment to extract gallium and germanium from where they have historically deposited the residue from its refining of zinc from five mines located in central and eastern Tennessee. The expected output is 30 tons of germanium and 40 tons of gallium a year—nearly making up for the 43.7 tons of germanium and 94 tons of gallium that China exported globally in 2022.9 The Round Top deposit in Texas is also a wonderful candidate for federal investment, particularly because it could co-produce multiple critical minerals from just one site.10 The government must incentivize initiatives like these to swiftly mitigate the economic and strategic losses resulting from China’s ban.

While there is an upper bound to direct sources of critical minerals domestically, advanced software and AI can expand our production potential. These technologies can identify previously overlooked commercial suppliers across the broader American Industrial Base who are already generating precursor elements with mineral companionality, but that aren’t yet integrated into defense supply chains. By mapping these untapped resources and connecting them with defense demand, we can identify commercial sector companies that could contribute to critical mineral production by extracting valuable byproducts that would otherwise remain unutilized. This data-driven approach to supplier discovery represents a lever to scale domestic production beyond existing defense contractors.

Investing domestically will not only stimulate recovery and enhance resilience in critical industries, but also position the United States to forge deeper international relationships. Such strategic investments enable the U.S. to develop stronger, long-term alliances, particularly with nations sharing common economic and security interests, such as Australia, to counter China’s expanding global influence.

Enhance National Stockpiles

In the meantime, there must be continued enhancement of strategic stockpiles. The National Defense Stockpile requires expansion to include adequate holdings of all affected minerals, with management practices aligned to both threat assessments and operational needs. For some minerals, it’s not even about expansion—it’s about inclusion. The 2024 report on gallium by the U.S. Geological Survey is explicit: “Government Stockpile: None.”11 The same can be said for tellurium in this year’s report.12

Five critical minerals—barite, cesium, rhodium, rubidium, and ruthenium—are notably absent from the “Materials of Interest” list for DLA Strategic Minerals.13 Given the significance assigned to these minerals by the U.S. Geological Survey (USGS), this inconsistency between the USGS’s assessments and the DLA’s strategic priorities effectively acknowledges a critical vulnerability and reliance without implementing adequate defenses to protect against exploitation.

Much of this paper focused specifically on the minerals currently restricted by China; however, if U.S. efforts are limited to reactionary measures alone, it will remain strategically vulnerable. Further Chinese measures are likely, as its dominance over the bedrock of our weapon systems extends far beyond just the minerals discussed above. Other key vulnerabilities include:

Magnesium: In 2024, China was the global leader in magnesia and magnesite production and the primary exporter of magnesia to the United States and numerous other nations. Magnesium, essential for aircraft frames, helicopter rotors, and missile casings, lacks any form of U.S. government stockpile.

Graphite: In 2024, China controlled nearly 80% of the world’s graphite production, supplying approximately 43% of U.S. imports. Graphite is crucial in rocket propulsion systems and military-grade batteries, yet again, the U.S. maintains no strategic stockpile.

Fluorspar: In 2024, China accounted for 62% of global fluorspar production. Despite its critical applications in precision lenses, laser technologies, semiconductor manufacturing, and nuclear fuel processing, the U.S. has failed to establish a reserve stockpile.14

These minerals share the same vulnerabilities as those already targeted by China—critical necessity combined with U.S. scarcity. Unless proactive measures are expanded, the United States risks continued strategic vulnerability due to its primary dependence on Chinese-controlled resources.

In an era where geopolitical power is increasingly defined as much by resource control as by military strength, America's dependence on China for critical minerals represents a glaring and growing strategic vulnerability. The complex journey from mineral extraction to weapon system deployment—from rock to rocket—is vital to national security yet it is severely compromised, posing substantial risks to U.S. defense capabilities.

China’s recent export bans and restrictions on critical minerals have exposed an open secret: despite political rhetoric, the United States is fundamentally dependent on China for essential components of its weapon systems. The data clearly demonstrates the extent of this dependence and highlighted the significant risks posed by these restrictions. While potential solutions have been outlined—and some are already in limited use—the current response remains limited relative to the scope of the challenge.

Addressing this challenge will require reimagining critical supply chains within America’s borders and among trusted allies. Increasing domestic production capabilities, effectively leveraging mineral companionality, and significantly expanding strategic stockpiles are essential first steps. These measures require aggressive scaling, sustained strategic investment, and a commitment to innovation and international collaboration to effectively find new levers against current vulnerabilities.

The United States faces a strategic decision: whether to continue relying on potentially hostile sources for the building blocks of military power, or decisively invest in securing these essential resources—ensuring the journey from rock to rocket remains secure, resilient, and within America's control.

1 USGS Mineral Commodity Summaries 2025

2 IM Mining: China Pursues Gold & Antimony Targets in Tajikistan

3 Foundry Planet: Rus Rotenberg to Establish Russia's Largest Antimony Production

4 The Economist: China Is Tightening Its Grip on the World's Minerals

5 Data subject to outlier filtering to ensure quality.

6 Utah's Kennecott Mine Recovers Tellurium for Green Energy Products

7 IGF: Searching for Critical Minerals? – How Metals are Produced and Associated Together

8 Perpetua Resources Receives up to an Additional $34.6 Million Under the Defense Production Act

9 VOA News: Tennessee Refinery Could Break Chinese Chokehold on Two Critical Minerals

10 USGS Updates Mineral Database with Gallium Deposits in the United States

11 The 2025 report (cited below) listed “Government Stockpile: Not Available.

12 USGS Mineral Commodity Summaries 2025

From raw minerals to advanced weapon systems—from rock to rocket—there lies a reality: America’s military superiority increasingly depends on China. China recently tightened its grip on critical minerals essential to defense and commercial technologies by expanding its export controls to include tungsten, tellurium, and other vital materials. This action builds upon earlier restrictions introduced in 2024, targeting gallium, germanium, and antimony.

China recently tightened its grip on critical minerals essential to defense and commercial technologies by expanding its export controls to include tungsten, tellurium, and other vital materials. This action builds upon earlier restrictions introduced in 2024, targeting gallium, germanium, and antimony.

Though these minerals rarely capture national attention, they underpin crucial components of America’s defense infrastructure. They are integral to radar systems that detect threats, night-vision equipment that provides tactical advantages, and precision-guided munitions essential to modern warfare. America’s heavy reliance on Chinese suppliers for these strategic resources poses a major national security risk.

Importance of These Critical Minerals

Antimony, gallium, germanium, tungsten, and tellurium each play specialized roles in military applications, ranging from flameresistant gear and advanced semiconductors to nuclear detection and hypersonic weaponry. These materials are indispensable for modern defense infrastructure, yet their supply chains remain vulnerable to geopolitical risks. The below examples underscore how these elements underpin foundational military capabilities.

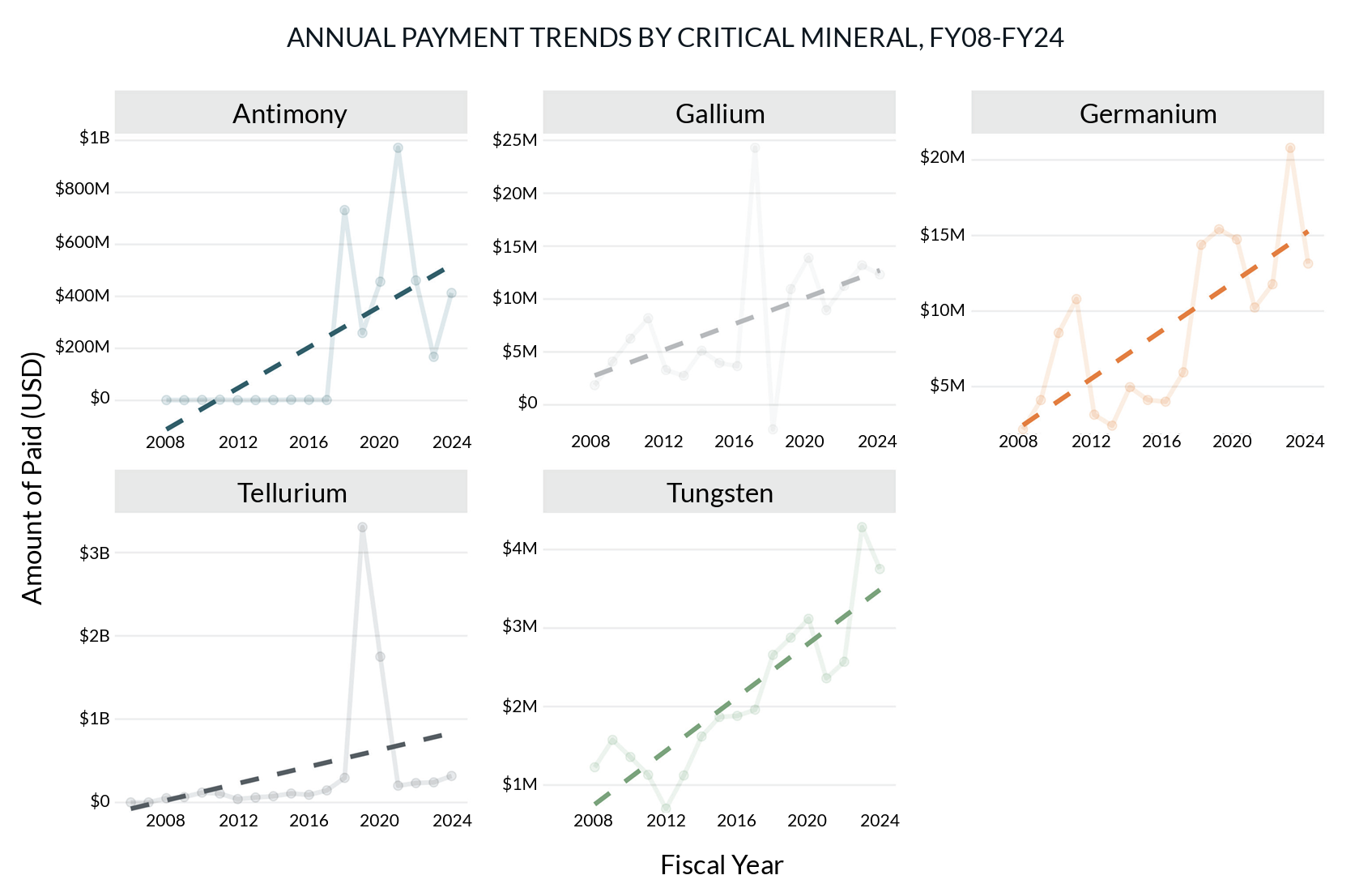

The export bans and controls come as DoD increases its demand for parts containing critical minerals to support the acquisition lifecycle of weapon systems. Since 2010, Department of Defense (DoD) contracts for components containing these five critical minerals have increased by an average of 23.2% per year (Figure 1) while the DoD’s spending on these components has grown by about 7% annually. The increases are larger within specific critical minerals —contracts for parts with gallium have surged by 41.8% each year, and spending on germanium-containing parts has risen by 16.1% year-over-year (Figure 2).

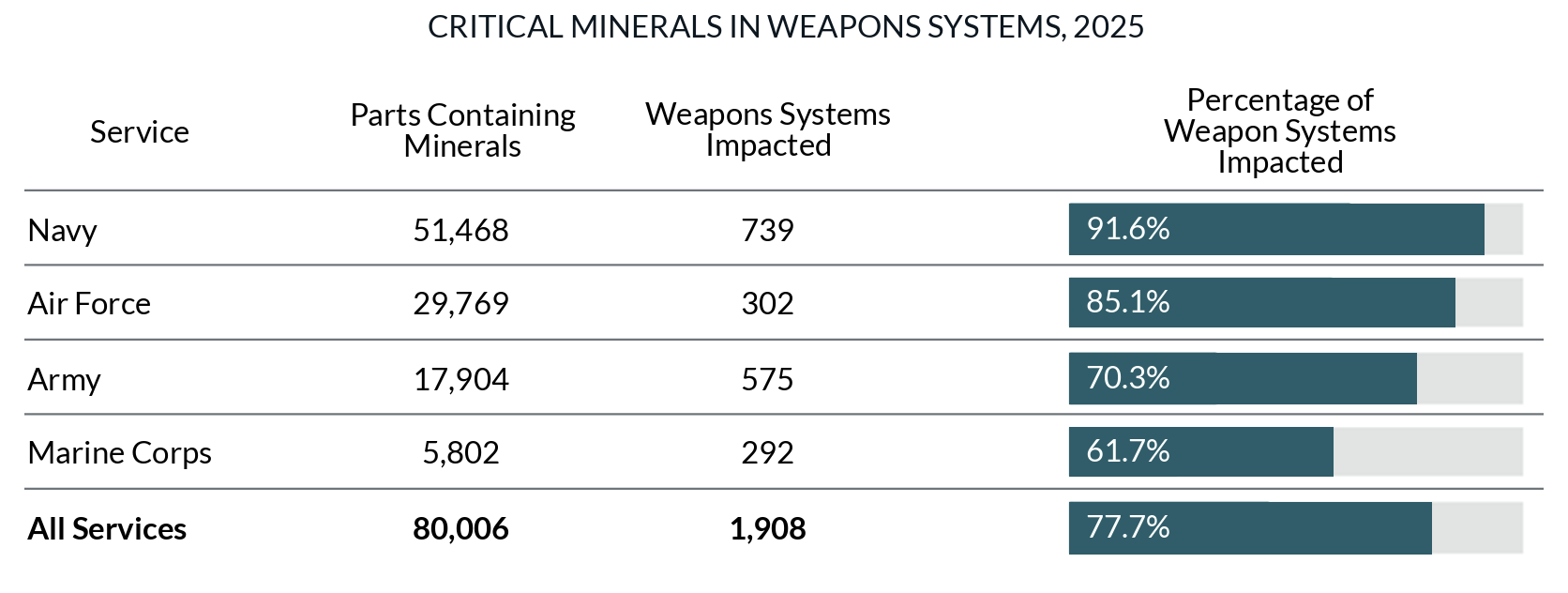

This upward trend of spending also reflects broader reliance on these minerals. More than 80,000 parts across 1,900 weapon systems incorporate antimony, gallium, germanium, tungsten, or tellurium, meaning nearly 78% of all DoD weapon systems are potentially affected. This dependence spans across the military services. Over 91% of Navy weapon systems rely on these materials, while 61.7% of Marine Corps systems rely on parts connected to these critical minerals (Figure 3). Some of the systems most impacted include the Arleigh Burke Class destroyers, America Class amphibious assault ships, Nimitz Class aircraft carriers, and the Minuteman III nuclear missile program.

The growing reliance on these critical minerals exacerbates concerns over supply chain stability and adversarial reliance.

The modernization of U.S. military capabilities and expanding operational demand is driving a significant increase in material consumption. But how does the U.S. secure these critical resources?

The journey—from extracting raw rock to deploying a fully assembled rocket— follows a complex network of suppliers, processors, and manufacturers that convert raw minerals into military-grade components. This process involves several key stages: mining the mineral, refining it, manufacturing the end product, and finally, distributing it to the Department of Defense. Every link in this chain must remain free from adversarial influence. For example, even if antimony is mined in Australia, if it is refined in China, the ban will prevent it from ever touching an American weapon system.

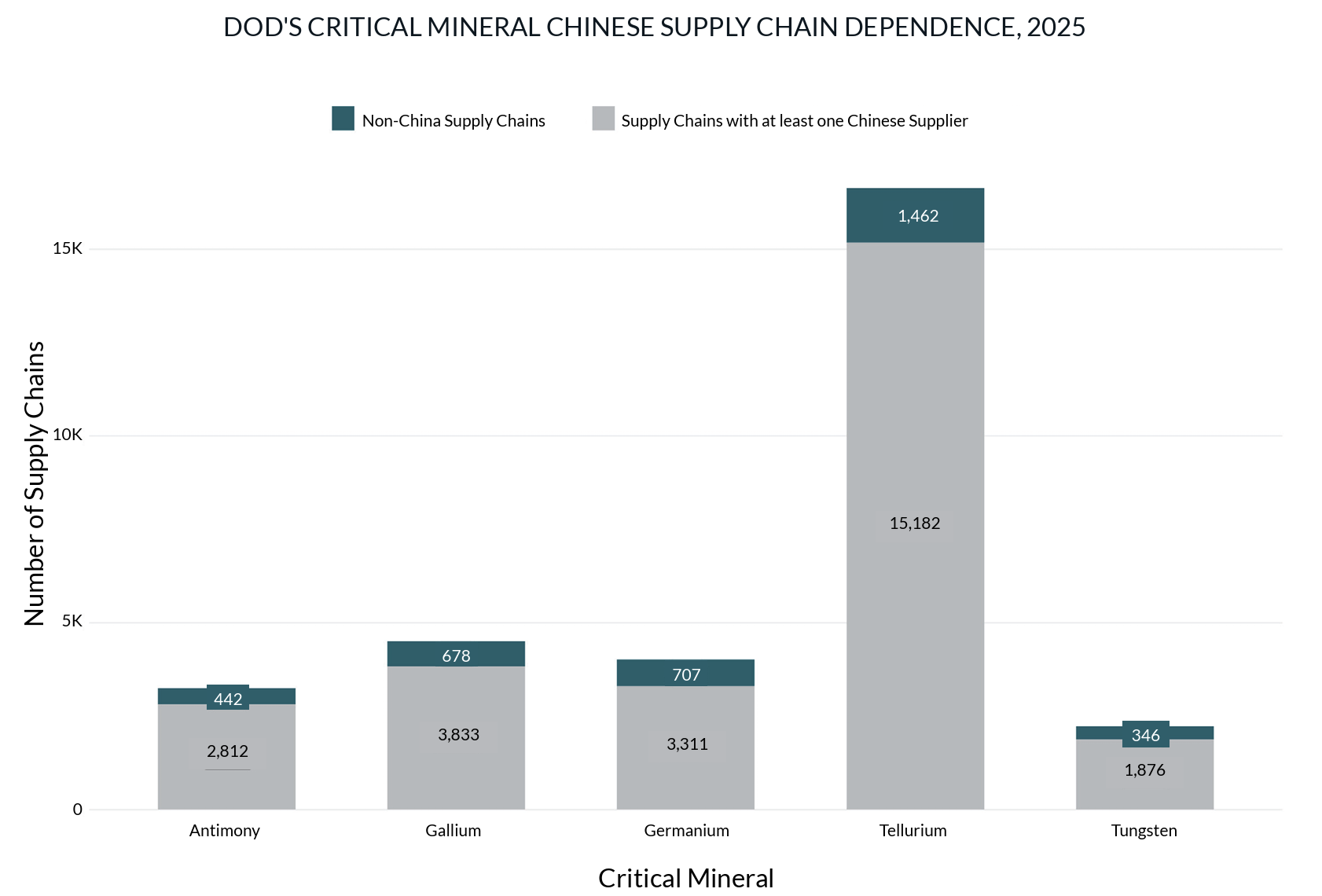

Over 43,000 different supply chains have some level of Chinese dependence extending down to six tiers of suppliers. This analysis identified all the potential ways that a mineral is refined, made into a part, and then procured by the Department of Defense to support the production of over 1,900 weapon systems. 88% of these supply chains are influenced by China and potentially jeopardized by the Chinese exit bans (Figure 4).

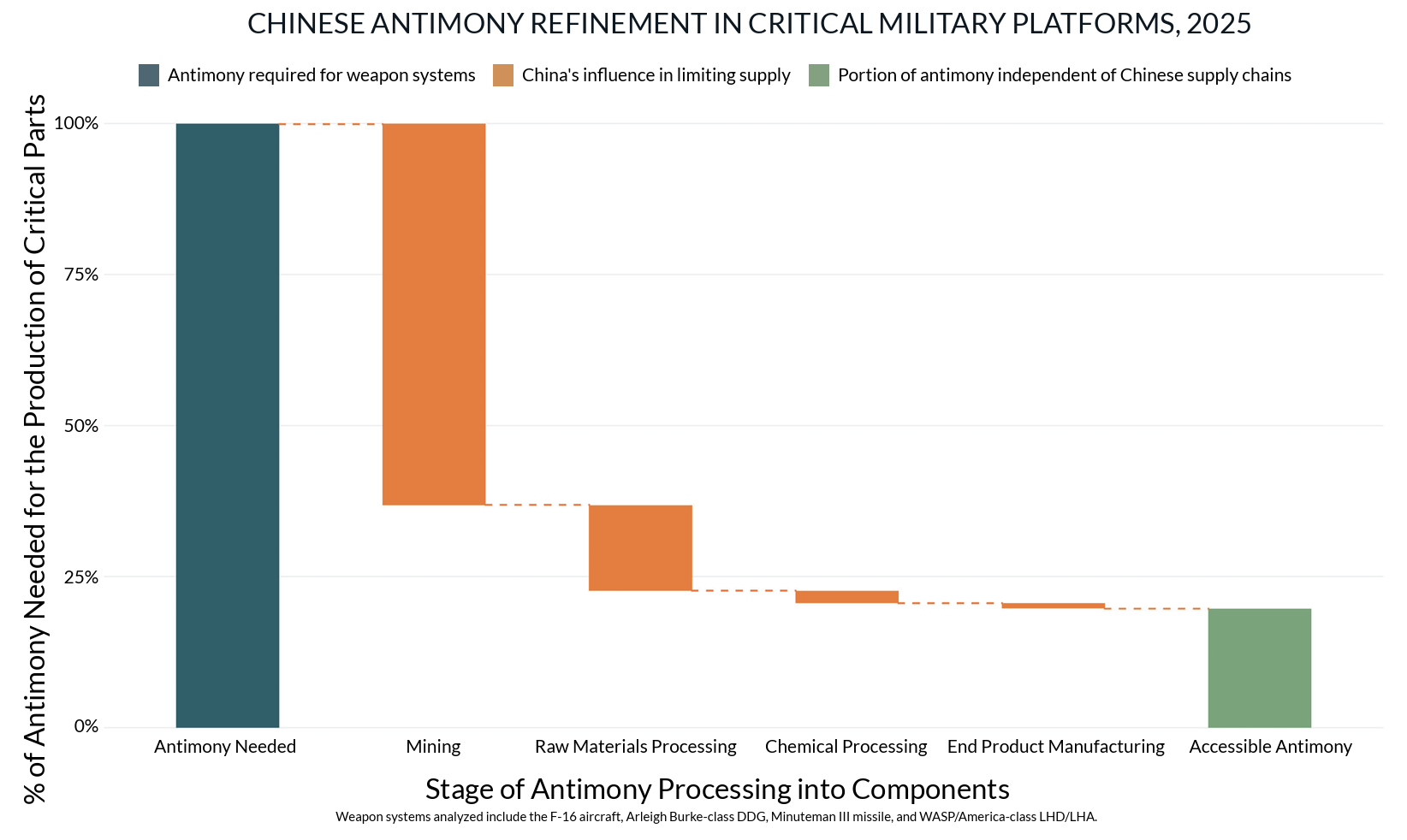

Let’s examine antimony’s role in four key weapon systems—the F-16 fighter jet, the Arleigh Burke-class destroyer, the Minuteman III missile, and the Wasp-class amphibious assault ship. Each platform represents decades of American innovation and meticulous engineering, and yet more than 80% of the antimony required for these systems is affected by the ban (Figure 5).

Most of the impact of the ban comes from China’s dominance in the mining sector, with roughly 60% of global antimony is mined in China.1 However, even if antimony is not mined in China, Chinese firms operate internationally to further entrench their mineral dominance. For example, Tibet Huayu, a subsidiary of China’s state-owned Tibet Mineral Development Co., operates the Anzob antimony-gold complex in Tajikistan through a $200 million joint venture with Tajik Aluminium Company (TALCO).2 Other countries with Chinese involvement in antimony mining are Russia3 and Ghana.4

China’s control over raw antimony processing, another step in the supply chain, further limits U.S. supply. Nearly one-third of antimony that was initially processed elsewhere ends up being refined in China. Combined with China’s extensive manufacturing capabilities, only 19% of the antimony needed for these weapon systems is available outside of China. This heavy reliance on Chinese-refined antimony not only exposes critical defense supply chains to potential political and economic leverage, but may also drive up costs and delay production timelines for U.S. military platforms.

We have already seen an impact on DoD procurement. In the three months following China’s export ban on antimony, gallium, and germanium, parts containing these critical minerals saw prices increase by an average of 5.2% after the ban, compared to procurements of those same parts the few months prior. More specifically, the price for components containing gallium increased by 6.0%, those with antimony by 4.5%, and germanium by 1.6%. All other parts increased by an average of only 1.4% (Figure 6).5

These figures not only reflect immediate market responses, but also signal the potential for more severe disruptions as the bans continue to influence global supply dynamics. As vendors begin to grapple with the indirect effects of these export restrictions, further price escalations are anticipated.

The data points to actionable solutions that can begin to address these strategic vulnerabilities.

Increase Domestic Capabilities

First, the United States must revive its domestic processing capabilities. Today, the United States exports raw precursors for more than 35 critical minerals to China to be processed before they are re-imported back. However, this cycle has been broken, as China now prevents exports of select critical minerals back to the United States. This dependency on foreign processing exposes our supply chains to geopolitical risk and undermines our economic sovereignty.

Addressing this challenge requires comprehensive mapping of material precursors and tax incentives that encourage private sector investment in domestic refining capabilities. While there has been progress—such as DoD investing $59.4 million under the Defense Production Act in February 2024 to support reserves in Idaho in an effort to boost domestic antimony production—there are still no domestic sources for gallium, germanium, or tungsten.

As an example, the United States has become a new producer of tellurium within the past three years. Working closely with the Department of Energy’s Critical Minerals Institute, private industry began extracting copper from the Kennecott mine in Utah, which has been instrumental in dropping the United States’ tellurium foreign reliance from 95% in 2019 down to 25% in 2023.6 The tellurium is refined in Canada then supplied to an American solar panel manufacturer. While we may not develop new domestic sources for every critical mineral, allied nations offer attractive augmentation of our supplies, from Australia antimony reserves to Canada’s refining capabilities.

Leverage Mineral Companionality

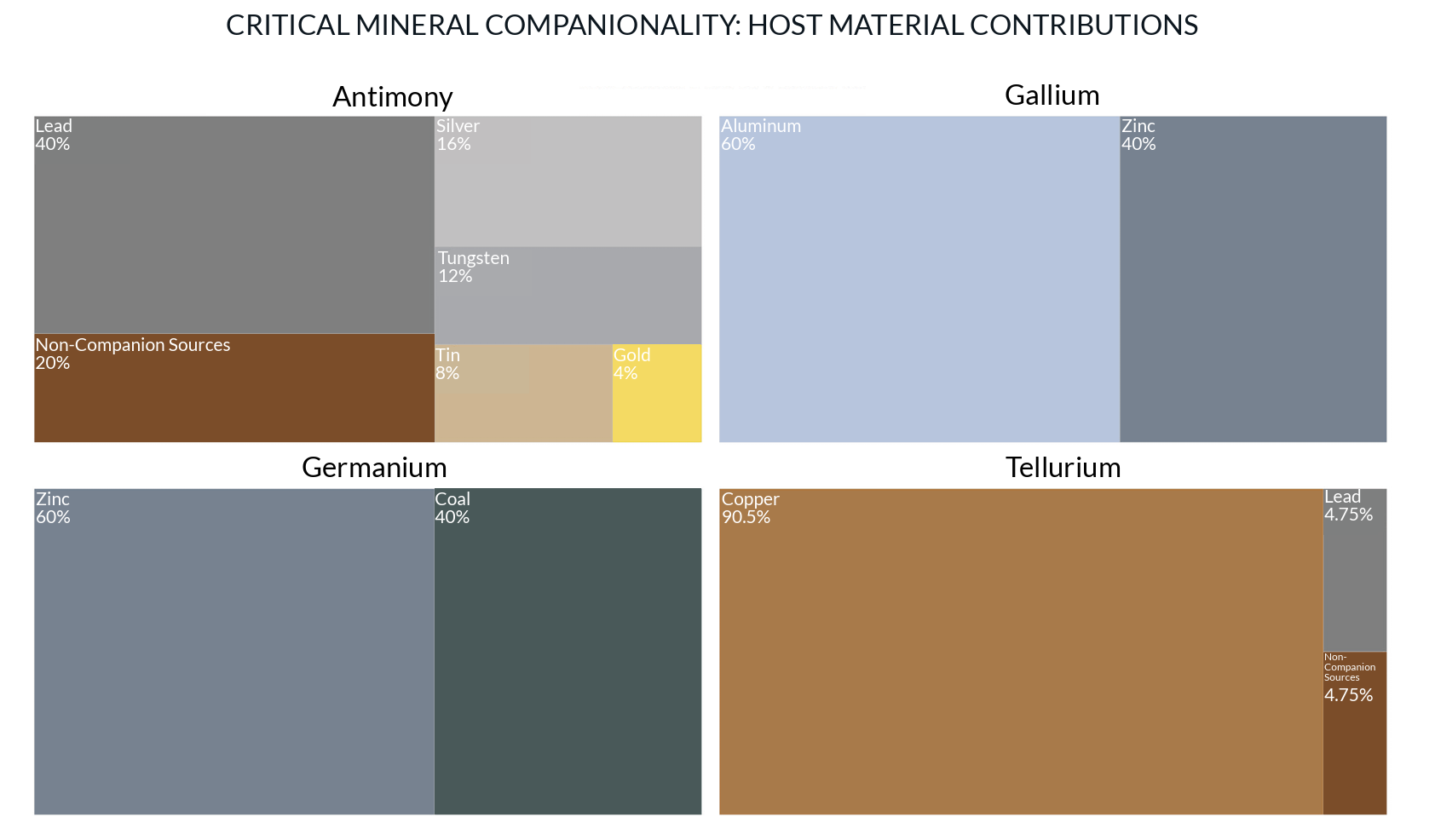

Material companionality is a critical yet overlooked factor shaping the viability of domestic mineral resources and national supply chain security. Pure critical minerals are rarely found in nature; instead, they usually appear alongside other materials in varying concentrations and smaller quantities. Consequently, sources of critical minerals exist within the United States and allied countries, yet these resources often remain unprocessed. Several factors contribute to this situation:

First, critical minerals within these mineral deposits frequently exist in low concentrations, requiring the processing of larger quantities of material to yield commercially viable amounts. This increased processing significantly raises operational costs, reducing profit margins and making extraction less economically appealing.

Second, extracting these metals from their associated minerals often necessitates advanced and costly extraction technologies. The substantial capital investments and high operating expenses required for such technologies can render domestic mineral processing economically unfeasible.

Finally, stringent licensing and permitting processes often hinder the extraction of companion minerals. Existing mining permits frequently authorize only the extraction of primary minerals, excluding secondary or companion minerals. Initiating extraction of additional minerals typically requires renewed regulatory discussions, extended governmental negotiations, and updated permits, further delaying production timelines.7

To address these challenges, the federal government should offer subsidies and contracts to incentivize companies to leverage mineral companionality. One example is the aforementioned effort in Idaho, where Perpetua Resources received up to $59 million under the Defense Production Act to redevelop an abandoned mining site. This funding specifically supports extracting antimony—a critical mineral previously overlooked due to its association with gold mining operations.8 Other efforts include the Netherlands-headquartered Nyrstar searching for government investment to extract gallium and germanium from where they have historically deposited the residue from its refining of zinc from five mines located in central and eastern Tennessee. The expected output is 30 tons of germanium and 40 tons of gallium a year—nearly making up for the 43.7 tons of germanium and 94 tons of gallium that China exported globally in 2022.9 The Round Top deposit in Texas is also a wonderful candidate for federal investment, particularly because it could co-produce multiple critical minerals from just one site.10 The government must incentivize initiatives like these to swiftly mitigate the economic and strategic losses resulting from China’s ban.

While there is an upper bound to direct sources of critical minerals domestically, advanced software and AI can expand our production potential. These technologies can identify previously overlooked commercial suppliers across the broader American Industrial Base who are already generating precursor elements with mineral companionality, but that aren’t yet integrated into defense supply chains. By mapping these untapped resources and connecting them with defense demand, we can identify commercial sector companies that could contribute to critical mineral production by extracting valuable byproducts that would otherwise remain unutilized. This data-driven approach to supplier discovery represents a lever to scale domestic production beyond existing defense contractors.

Investing domestically will not only stimulate recovery and enhance resilience in critical industries, but also position the United States to forge deeper international relationships. Such strategic investments enable the U.S. to develop stronger, long-term alliances, particularly with nations sharing common economic and security interests, such as Australia, to counter China’s expanding global influence.

Enhance National Stockpiles

In the meantime, there must be continued enhancement of strategic stockpiles. The National Defense Stockpile requires expansion to include adequate holdings of all affected minerals, with management practices aligned to both threat assessments and operational needs. For some minerals, it’s not even about expansion—it’s about inclusion. The 2024 report on gallium by the U.S. Geological Survey is explicit: “Government Stockpile: None.”11 The same can be said for tellurium in this year’s report.12

Five critical minerals—barite, cesium, rhodium, rubidium, and ruthenium—are notably absent from the “Materials of Interest” list for DLA Strategic Minerals.13 Given the significance assigned to these minerals by the U.S. Geological Survey (USGS), this inconsistency between the USGS’s assessments and the DLA’s strategic priorities effectively acknowledges a critical vulnerability and reliance without implementing adequate defenses to protect against exploitation.

Much of this paper focused specifically on the minerals currently restricted by China; however, if U.S. efforts are limited to reactionary measures alone, it will remain strategically vulnerable. Further Chinese measures are likely, as its dominance over the bedrock of our weapon systems extends far beyond just the minerals discussed above. Other key vulnerabilities include:

Magnesium: In 2024, China was the global leader in magnesia and magnesite production and the primary exporter of magnesia to the United States and numerous other nations. Magnesium, essential for aircraft frames, helicopter rotors, and missile casings, lacks any form of U.S. government stockpile.

Graphite: In 2024, China controlled nearly 80% of the world’s graphite production, supplying approximately 43% of U.S. imports. Graphite is crucial in rocket propulsion systems and military-grade batteries, yet again, the U.S. maintains no strategic stockpile.

Fluorspar: In 2024, China accounted for 62% of global fluorspar production. Despite its critical applications in precision lenses, laser technologies, semiconductor manufacturing, and nuclear fuel processing, the U.S. has failed to establish a reserve stockpile.14

These minerals share the same vulnerabilities as those already targeted by China—critical necessity combined with U.S. scarcity. Unless proactive measures are expanded, the United States risks continued strategic vulnerability due to its primary dependence on Chinese-controlled resources.

In an era where geopolitical power is increasingly defined as much by resource control as by military strength, America's dependence on China for critical minerals represents a glaring and growing strategic vulnerability. The complex journey from mineral extraction to weapon system deployment—from rock to rocket—is vital to national security yet it is severely compromised, posing substantial risks to U.S. defense capabilities.

China’s recent export bans and restrictions on critical minerals have exposed an open secret: despite political rhetoric, the United States is fundamentally dependent on China for essential components of its weapon systems. The data clearly demonstrates the extent of this dependence and highlighted the significant risks posed by these restrictions. While potential solutions have been outlined—and some are already in limited use—the current response remains limited relative to the scope of the challenge.

Addressing this challenge will require reimagining critical supply chains within America’s borders and among trusted allies. Increasing domestic production capabilities, effectively leveraging mineral companionality, and significantly expanding strategic stockpiles are essential first steps. These measures require aggressive scaling, sustained strategic investment, and a commitment to innovation and international collaboration to effectively find new levers against current vulnerabilities.

The United States faces a strategic decision: whether to continue relying on potentially hostile sources for the building blocks of military power, or decisively invest in securing these essential resources—ensuring the journey from rock to rocket remains secure, resilient, and within America's control.

1 USGS Mineral Commodity Summaries 2025

2 IM Mining: China Pursues Gold & Antimony Targets in Tajikistan

3 Foundry Planet: Rus Rotenberg to Establish Russia's Largest Antimony Production

4 The Economist: China Is Tightening Its Grip on the World's Minerals

5 Data subject to outlier filtering to ensure quality.

6 Utah's Kennecott Mine Recovers Tellurium for Green Energy Products

7 IGF: Searching for Critical Minerals? – How Metals are Produced and Associated Together

8 Perpetua Resources Receives up to an Additional $34.6 Million Under the Defense Production Act

9 VOA News: Tennessee Refinery Could Break Chinese Chokehold on Two Critical Minerals

10 USGS Updates Mineral Database with Gallium Deposits in the United States

11 The 2025 report (cited below) listed “Government Stockpile: Not Available.

12 USGS Mineral Commodity Summaries 2025